WhatsApp’s Unexpected Journey in Brazil with Pix

Hey Payments Fanatic!

Ever wonder how WhatsApp carved out its spot in Brazil’s payment scene? It all started with a clever pivot around Pix, setting the stage for something big.

When WhatsApp initially entered the payments space in 2020, its launch had to be reworked following the Central Bank of Brazil’s introduction of Pix. WhatsApp rolled out its service in stages, gradually adapting and aligning with the country’s instant payment system instead of competing with it.

By 2021, P2P transactions via WhatsApp Pay were approved, followed by retail payments in 2023. Recently, the platform enabled users to link their Pix key directly within the app, further embedding itself into the financial routines of millions of Brazilians.

“We never wanted to compete with Pix,” explains Guilherme Horn, WhatsApp’s head for Brazil, India, and Indonesia. “We pivoted. We started with credit cards, but once we introduced Pix, adoption was remarkable.”

This shift in strategy has positioned WhatsApp as an enabler, not a disruptor, strengthening its ties with banks and fintechs. Today, institutions of all sizes, from traditional banks to digital-first startups, rely on WhatsApp as a core channel for transactions, lending, and debt management.

The rise of generative AI is further accelerating this trend, making interactions through text, audio, and voice more seamless than ever. In fact, conversion rates on WhatsApp have been reported to be up to 40 times higher than traditional channels like call centers, email, SMS, or apps.

Looking ahead, the next phase of this evolution points to a smoother financial journey powered by Open Finance. While still in its testing phase, the objective is clear: to allow users to complete financial transactions entirely within WhatsApp, removing the need to jump between platforms.

If you’re interested in reading a bit about what’s been happening in Payments, keep scrolling!

Cheers,

INSIGHTS

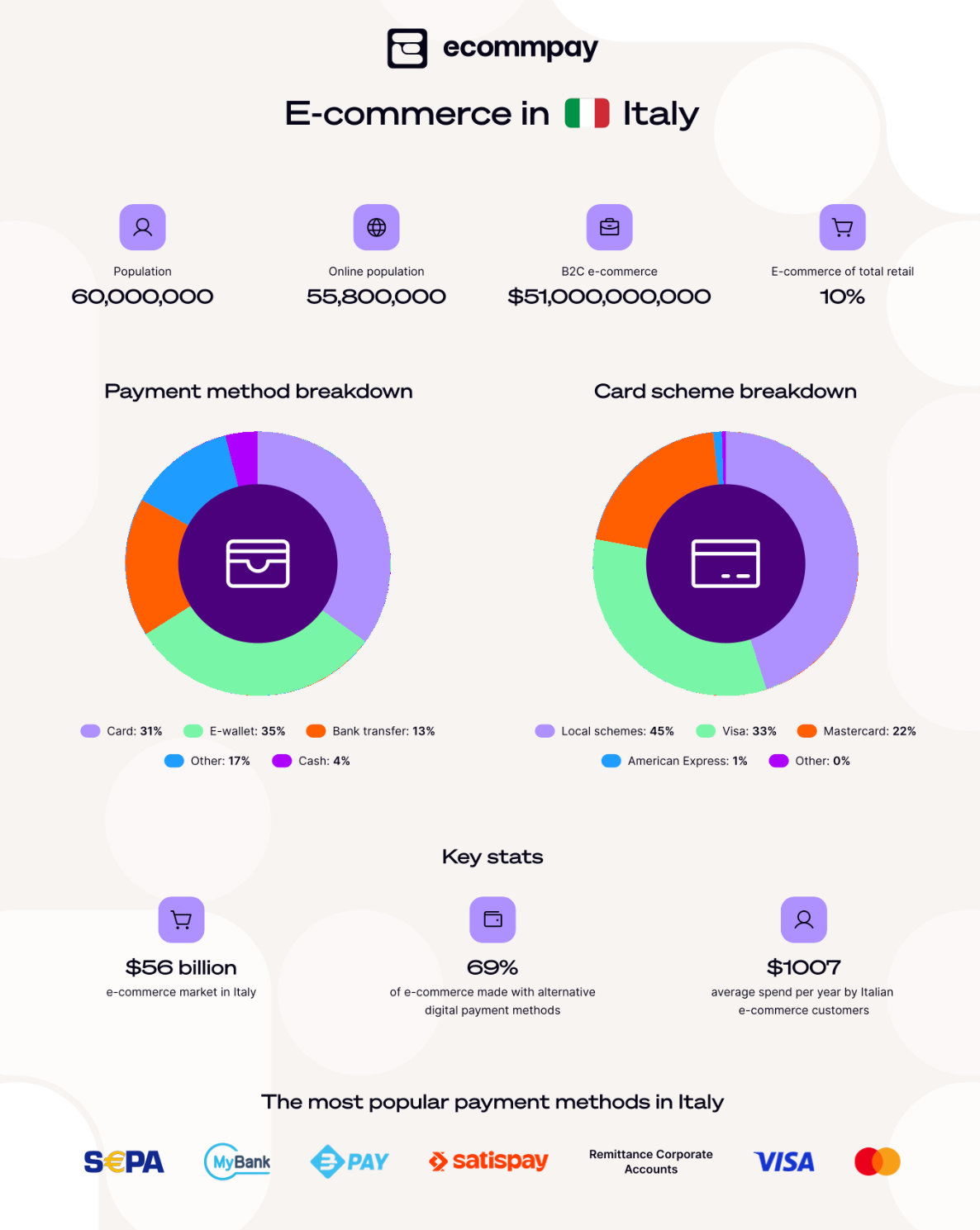

🇮🇹 The most popular payment methods in Italy, by Ecommpay. Cash remains a popular way to pay, but several factors are driving the swift growth of e-commerce in the region.

PAYMENTS NEWS

🇬🇧 Temu expands partnership with Checkout.com to enhance digital payments experience for online shoppers. Customers will have a smoother checkout experience thanks to Checkout.com’s global payment network. The company will now handle payments in over 30 markets, supporting a wide range of payment options from major credit cards.

🇺🇸 ACI Worldwide and Ingo Payments to power faster, flexible digital disbursements. The companies have announced ACI Speedpay Digital Disbursements, a new value-added feature within the ACI Speedpay platform, designed to help businesses scale their disbursement operations efficiently to meet customer expectations and evolving regulatory standards.

🇸🇬 Confide Platform launches Startup Compliance. The platform helps founders quickly build trust with customers, investors, and regulators. It allows startups to quickly create investor-ready compliance programs while showing the operational integrity needed to secure important customer contracts.

🌍 Tap to Pay on iPhone is now available with Mollie in Poland, Portugal, Switzerland and Finland. Users can accept all types of in-person, contactless payments directly on their iPhone, without the need for additional hardware. This feature helps businesses reach new customers, simplify checkout, process payments on the go, and explore setups like line busting.

🌍 Apple introduces Tap to Pay on iPhone in more European countries. Now available in Bulgaria, Finland, Hungary, Liechtenstein, Poland, Portugal, Slovakia, Slovenia, and Switzerland, it enables millions of merchants to use iPhone to securely accept in-person, contactless payments. It works closely with payment platforms like Adyen, myPOS, Revolut, Viva, Nexi, and app developers across the payments and commerce industry.

🇪🇸 Revolut becomes a collaborator entity of the State Tax Administration Agency. This will allow Revolut customers to pay their taxes directly through the AEAT website by selecting Revolut as a payment option, as well as to set up direct debits or manage self-assessments through the platform itself.

🇬🇧 World’s first online card-present transaction marks a major milestone in the evolution of payments. This advancement brings tap and PIN into the online world. The payment solution, developed by Welsh company Burbank, enables merchants to securely process card-present transactions in online channels.

🇬🇧 Capital On Tap selects GoCardless for variable recurring payments. Customers will be able to repay their credit cards every month using Direct Debit, and have the option to make weekly repayments and recurring payments for variable amounts through open banking.

🇦🇺 Visa joins forces with Australian banks on B2B payments. Australian business owners using the SAP platform will be able to route commercial payments to all suppliers, including those that don’t accept card payments. Visa also plans to add other local partners in the future.

🇨🇦 FinTech Nium expands real-time payments network with addition of Interac in Canada. With Interac, Nium’s customers can now access one of Canada’s most widely-used payment networks, “enabling real-time cross-border transfers to individuals and businesses nationwide in Canadian dollars.”

🇮🇳 Pine Labs prepares for major IPO, aiming to raise $1 billion despite the lukewarm market conditions in the country. Pine Labs' planned move to solidify its roots in India signals its dedication to expanding its array of tech solutions for banks and businesses.

🇪🇸 Deutsche Bank launches Bizum for businesses in Spain. Foreign multinationals with a presence in Spain and national businesses that have a virtual POS service associated with Deutsche Bank, will be able to accept payment by bizum in their electronic businesses.

🇺🇸 Affirm comments on Klarna, OnePay taking over BNPL service for Walmart. A spokesperson from Affirm stated: “We win business when merchants want superior performance and maximum value, given our underwriting and capital markets advantages. We will continue our long-term strategy of competing on our products and entering into sustainable partnerships.”

GOLDEN NUGGET

Welcome to 𝐓𝐡𝐞 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐀𝐜𝐚𝐝𝐞𝐦𝐲 by Checkout.com — Episode 6 👋

𝐓𝐡𝐞 𝐓𝐲𝐩𝐞𝐬 𝐨𝐟 𝐅𝐫𝐚𝐮𝐝 𝐢𝐧 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬:

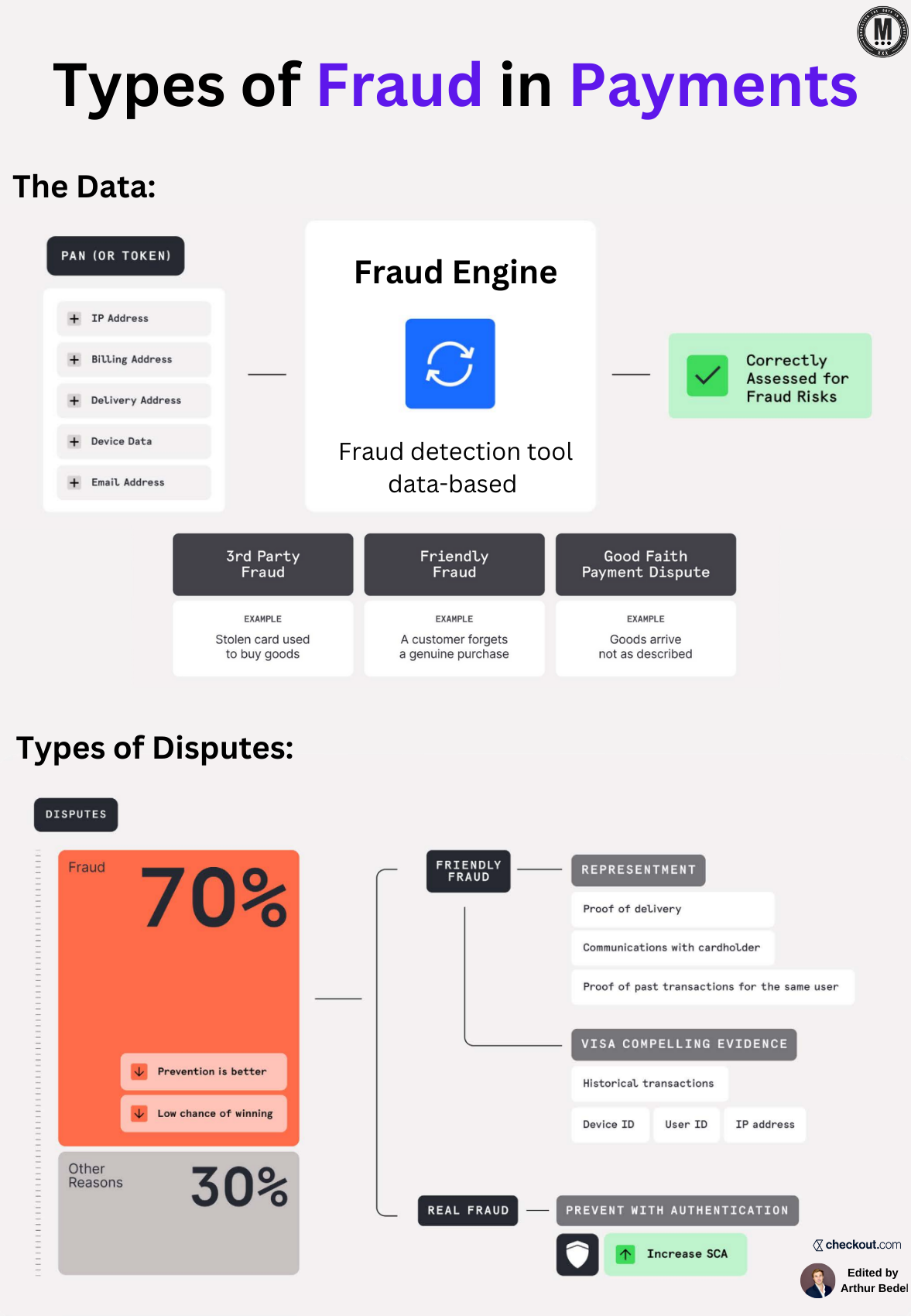

► Fraud in payments is a growing challenge for merchants, issuers, and payment processors. Fraudulent transactions not only cause financial losses but also damage a merchant’s reputation

► To combat fraud effectively, businesses must leverage fraud detection tools, authentication techniques, and dispute management strategies to stay ahead of bad actors while maintaining a seamless customer experience

𝐓𝐡𝐞 𝐓𝐲𝐩𝐞𝐬 𝐨𝐟 𝐅𝐫𝐚𝐮𝐝 & 𝐄𝐱𝐚𝐦𝐩𝐥𝐞𝐬

► 3-𝐏𝐚𝐫𝐭𝐲 𝐅𝐫𝐚𝐮𝐝 – This occurs when a fraudster uses stolen card details to make purchases.

► 𝐅𝐫𝐢𝐞𝐧𝐝𝐥𝐲 𝐅𝐫𝐚𝐮𝐝 – A cardholder disputes a legitimate transaction, either by mistake or to reverse a purchase.

► 𝐆𝐨𝐨𝐝 𝐅𝐚𝐢𝐭𝐡 𝐏𝐚𝐲𝐦𝐞𝐧𝐭 𝐃𝐢𝐬𝐩𝐮𝐭𝐞𝐬 – The customer disputes a payment due to issues with product quality or fulfillment.

Fraud prevention strategies must be tailored to identify, assess, and respond to these types of fraud in real time.

𝐓𝐡𝐞 𝐏𝐫𝐨𝐜𝐞𝐬𝐬: 𝐂𝐮𝐭𝐭𝐢𝐧𝐠 𝐃𝐨𝐰𝐧 𝐨𝐧 𝐂𝐚𝐫𝐝 𝐅𝐫𝐚𝐮𝐝

1️⃣ 𝐅𝐫𝐚𝐮𝐝 𝐃𝐞𝐭𝐞𝐜𝐭𝐢𝐨𝐧 𝐄𝐧𝐠𝐢𝐧𝐞𝐬 – These tools analyze transaction data (e.g., IP addresses, device data...) to assess fraud risks.

2️⃣ 3𝐃 𝐒𝐞𝐜𝐮𝐫𝐞 𝐀𝐮𝐭𝐡𝐞𝐧𝐭𝐢𝐜𝐚𝐭𝐢𝐨𝐧 – Adds an extra layer of protection by requiring customer verification for high-risk transactions.

3️⃣ 𝐌𝐚𝐜𝐡𝐢𝐧𝐞 𝐋𝐞𝐚𝐫𝐧𝐢𝐧𝐠 & 𝐀𝐈 – Predicts fraud patterns based on historical transactions and behavioral analytics.

4️⃣ 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 – Converts sensitive payment data into tokens, reducing the risk of stolen card details being misused.

5️⃣ 𝐂𝐡𝐚𝐫𝐠𝐞𝐛𝐚𝐜𝐤 𝐏𝐫𝐞𝐯𝐞𝐧𝐭𝐢𝐨𝐧 – Strategies like real-time alerts and clear billing descriptors

𝐓𝐡𝐞 𝐃𝐚𝐭𝐚: 𝐊𝐞𝐲 𝐃𝐚𝐭𝐚 𝐏𝐨𝐢𝐧𝐭𝐬 𝐭𝐨 𝐑𝐞𝐝𝐮𝐜𝐞 𝐅𝐫𝐚𝐮𝐝

Fraud detection relies on rich transaction data to identify suspicious activity and block fraudulent payments:

► Customer Name – Verifies the cardholder’s identity and checks for patterns of fraudulent behavior (e.g., fake names...).

► IP Address – Flags transactions from high-risk regions or locations inconsistent with the customer’s normal behavior.

► Billing Address – Used for Address Verification System (AVS) checks to confirm that the billing address matches the cardholder’s bank records.

► Delivery Address – Helps detect fraudulent transactions by assessing mismatched shipping details.

► Email Address – Identifies fraud patterns, such as disposable email addresses or emails associated with prior chargebacks.

Providing complete and accurate data in payment requests enhances fraud detection and reduces false declines, improving both security and conversion rates.

Source: Checkout.com x Connecting the dots in payments...

I highly recommend following my partner Arthur Bedel 💳 ♻️ for more great content like this one👌

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()