Viva Wallet vs JPMorgan: A Legal Standoff

Hey Payments Fanatic!

The dispute between Viva Wallet and JPMorgan has reached a critical stage, with CEO Haris Karonis filing an injunction to halt further lawsuits and takeover attempts by the US bank. The legal battle stems from JPMorgan’s 48.5% stake acquisition in 2022, which later unraveled into a series of lawsuits between the two parties.

“It is regrettable that ever since becoming a minority shareholder in Viva, JPMorgan has acted like a fox in a henhouse rather than seeking to prioritise Viva’s growth and success,” Karonis told Sifted.

At the heart of the conflict is a clause stating that WRL, Karonis’ holding company, would forfeit its right to reject a takeover if Viva Wallet’s valuation fell below €5bn by July 2025. Allegations from both sides range from obstruction of growth to unauthorized business decisions.

JPMorgan has taken the fight to courts in both Greece and the UK, seeking damages and alleging breaches of shareholder agreements. Meanwhile, its bid to overturn a ruling limiting its acquisition rights has been rejected. Will JPMorgan step back, or will WRL be the one to yield?

If you’re interested in reading a bit about what’s been happening in Payments, keep scrolling!

Cheers,

INSIGHTS

🇺🇸 80% of pay-by-bank users report better data security and lower cart abandonment. These benefits are especially important for retail, grocery, betting, ridesharing, telecommunications and utilities sectors, where user experience and security are top priorities. Despite the benefits, cost concerns remain a barrier to the wider adoption of pay by bank.

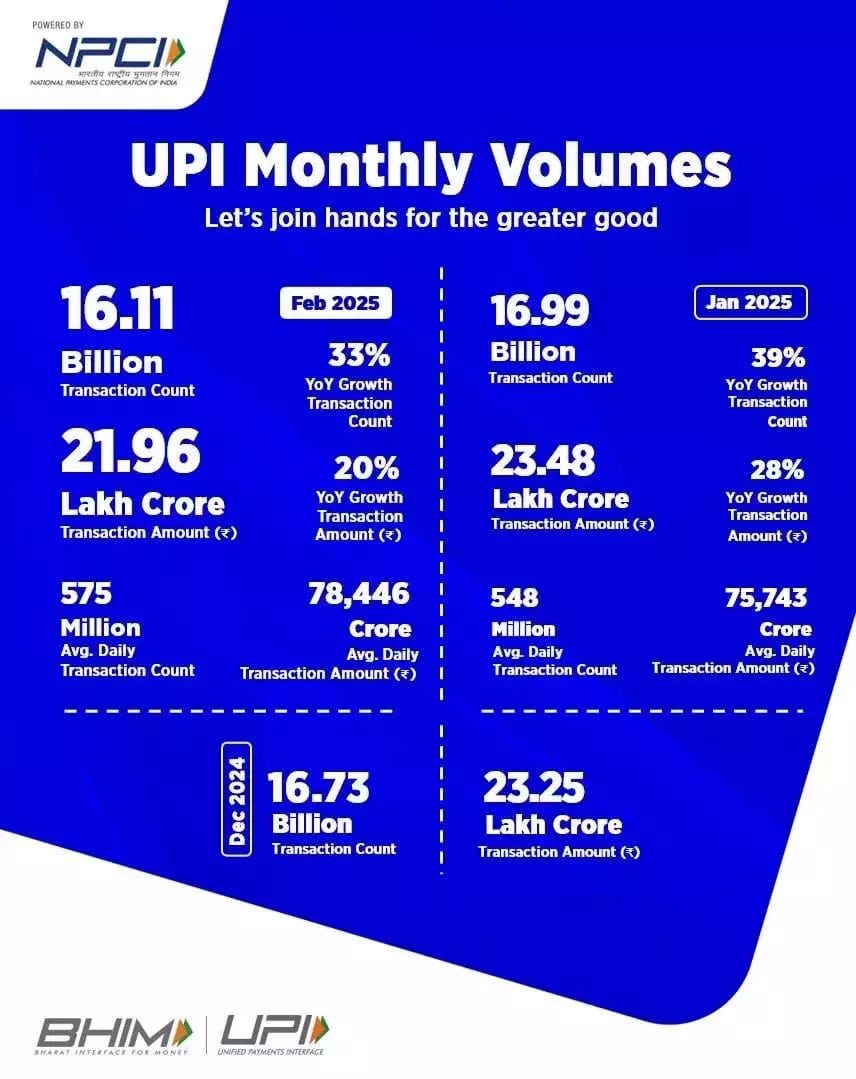

📊 UPI clocks 𝟱𝟳𝟱 𝗺𝗹𝗻 daily transactions and records 𝟭𝟲.𝟭𝟭 𝗕𝗻 volume in February 2025 🤯

PAYMENTS NEWS

➡️ Athia, DEUNA’s Aware AI, Presents Payment Optimization: Maximizing Bottom-Line Impact in Real Time.

Athia Reinventing Payment Strategy with AI

🇪🇪 How to avoid chargebacks on PayPal: A merchant’s guide by Solidgate. PayPal's unpredictable chargeback process can escalate quickly, pushing even low-risk merchants over thresholds. This guide explains how PayPal chargebacks work, why they happen, and how to prevent them.

🇺🇸 Confide rebrands to Confide Platform, delivering a complete GRC workflow and case management system. It also provides tailored solutions for startup and enterprise compliance. CEO Pav Gill aims to simplify compliance, enabling businesses to manage risk with an intuitive, all-in-one platform. Read on

🇺🇸 Ingo Payments partners with Securely to deliver real-time merchant settlements with advanced ledgering and payment capabilities. This collaboration marks a significant milestone for both companies as Securely™ partners to bring Ingo’s full-service embedded banking platform to the market, combining proven payment infrastructure with an innovative approach to real-time merchant settlement through advanced ledgering and diverse payment options.

🇲🇽 Kushki expands into Mexico and Colombia through a partnership with JP Morgan Payments. The collaboration aims to leverage JP Morgan’s network and expertise in payment processing while integrating Kushki’s acquiring services to enhance payment efficiency for businesses.

🇨🇴 Nu Colombia has partnered with Redeban, enabling over 2.5 million users to send and receive instant and free money transfers to and from any bank or digital wallet connected to the network in the country. This includes Bancolombia, Davivienda, Nequi, and Daviplata.

🇨🇦 Barclays closes in on sale of merchant acquiring business. The bank said in February that it was exploring a sale or partnership for the merchant acquiring division, which has struggled to remain competitive in the face of increasing competition.

🇨🇦 Best Buy Canada selects PingPong as their first cross-border partner. Best Buy will begin expanding internationally and facilitate payouts to international sellers. By leveraging PingPong's global capability, it will have the opportunity to unlock new revenue streams and cross-border operational efficiencies.

🇸🇦 Visa launches Tap to Add card in Saudi Arabia and Egypt. This enables cardholders to seamlessly add their cards to digital wallets by simply tapping them on their mobile device. Upon tapping, a unique one-time code validated by Visa's Chip Authenticate service, ensuring secure provisioning of card credentials and offering a significantly faster and more secure alternative to traditional methods.

🇬🇧 Mastercard and Visa linked to illegal gambling sites accused of scamming UK customers. An investigation has found that the payment giants are failing to stop their networks being used to make transactions on unlicensed sites despite a previous pledge to do so.

🇦🇪 FinTech Galaxy and ProgressSoft join forces to advance open banking in MENA. This collaboration enables banks, payment service providers (PSPs), and regulators to streamline compliance, enhance digital transactions, and build scalable financial ecosystems.

🇪🇬 Careem Pay launches money transfers to Egypt. The payments platform within the Careem app, expands its remittance service to the country, allowing UAE residents to send money directly to bank accounts in Egypt quickly and at competitive rates.

🇦🇷 Prepaid card transactions in Argentina grew by 39% during 2024. According to the fourth edition of GP Insight on the FinTech ecosystem in the country, prepaid cards have solidified as a growing payment method, with a significant increase in transaction volume and the number of transactions.

🇸🇪 Sweden's Riksbank works on offline payments in contingency planning for war outbreak. The possibility to pay offline in Sweden when the Internet is down is currently limited and does not work at all for contactless and mobile wallet payments. Learn more

🇺🇸 Splitit partners with Highnote to enable installment payments for digital wallet credit cards and merchant endpoints. This allows shoppers to use an existing credit card at checkout. Splitit’s unique installment payment option will now be available through a digital wallet at the point of sale.

🇺🇸 Astrada emerges from stealth to unveil a unified API for transaction data that offers the infrastructure, compliance, and workflows that software companies need to offer bring-your-own-card functionality. Using its API, software companies enable businesses to enroll Visa or Mastercard cards and track spending in real time.

🇸🇪 Zimpler partners with Swish to unlock direct participation. Through Zimpler’s direct participation, businesses can now integrate Swish faster, at a lower cost, and with greater stability. Explore more

🇧🇬 Bulgarian national payment operator BORICA implements Tips connectivity module from Montran. This solution enables banks to access TIPS, the ECB's instant payments service, integrating with Bulgaria's BISERA, and also includes advanced liquidity monitoring and controls.

🇪🇬 TerraPay teams up with Banque du Caire to optimise remittance payouts in Egypt. Through this move, both intend to enable digital payouts to all bank accounts and mobile wallets across the region, in turn delivering more efficient, cost-effective, and secure remittance services for the Egyptian diaspora globally.

GOLDEN NUGGET

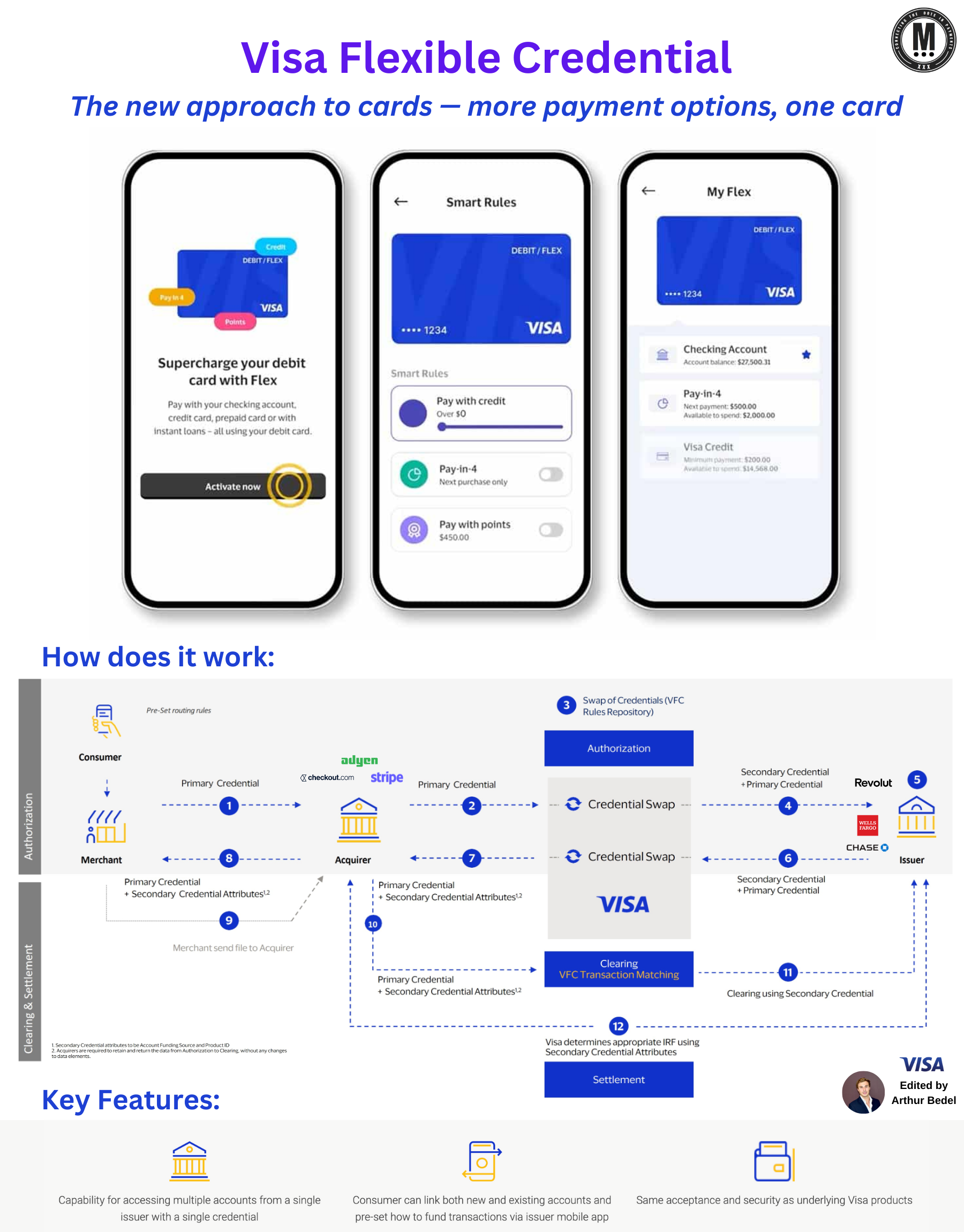

Visa 𝐅𝐥𝐞𝐱𝐢𝐛𝐥𝐞 𝐂𝐫𝐞𝐝𝐞𝐧𝐭𝐢𝐚𝐥 — The new approach to cards, more payment options, more funding sources, one credential

In today’s fast-evolving digital landscape, Visa's Flexible Credential is redefining how consumers access funds. This innovative solution enables users to link multiple funding sources — like credit, debit, or loyalty points — to a 𝐬𝐢𝐧𝐠𝐥𝐞 𝐩𝐚𝐲𝐦𝐞𝐧𝐭 𝐜𝐫𝐞𝐝𝐞𝐧𝐭𝐢𝐚𝐥, allowing them to switch between accounts seamlessly during transactions.

No more carrying multiple cards or worrying about balances on different accounts; a single card or digital credential can now serve as a gateway to multiple accounts, simplifying transactions for consumers and businesses alike.

► 𝐇𝐨𝐰 𝐈𝐭 𝐖𝐨𝐫𝐤𝐬

Visa Flexible Credential leverage Visa’s robust infrastructure to enable real-time access to various funding sources. For example, at checkout, if a primary account lacks sufficient funds, users can instantly switch to another linked source, such as loyalty points or a credit line. This flexibility is managed through the issuer’s app, giving consumers control over how they fund their transactions without having to start over or reauthorize purchases.

► 𝐓𝐡𝐞 𝐏𝐫𝐨𝐜𝐞𝐬𝐬

1️⃣ 𝐋𝐢𝐧𝐤 𝐌𝐮𝐥𝐭𝐢𝐩𝐥𝐞 𝐀𝐜𝐜𝐨𝐮𝐧𝐭𝐬 𝐭𝐨 𝐎𝐧𝐞 𝐂𝐫𝐞𝐝𝐞𝐧𝐭𝐢𝐚𝐥 Consumers link various accounts — such as debit, credit, loyalty points, or installment options — to a single Visa credential.

2️⃣ 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧 𝐈𝐧𝐢𝐭𝐢𝐚𝐭𝐢𝐨𝐧 At the point of sale (POS) or within an e-commerce platform, the user selects their Visa credential as the payment method.

3️⃣ 𝐀𝐜𝐜𝐨𝐮𝐧𝐭 𝐒𝐰𝐢𝐭𝐜𝐡𝐢𝐧𝐠 𝐯𝐢𝐚 𝐌𝐨𝐛𝐢𝐥𝐞 𝐀𝐩𝐩 If the initial, primary account lacks sufficient funds, the user can, through the app, immediately select an alternate funding source

4️⃣ 𝐕𝐢𝐬𝐚’𝐬 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐜𝐞𝐬𝐬𝐞𝐬 𝐭𝐡𝐞 𝐑𝐞𝐪𝐮𝐞𝐬𝐭 Visa’s backend processes the funding switch in real-time. This infrastructure is designed to route and authorize payments based on the selected funding source

5️⃣ 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧 𝐂𝐨𝐦𝐩𝐥𝐞𝐭𝐢𝐨𝐧 Once the preferred account is selected, the transaction proceeds as usual, with funds drawn from the designated source.

The Visa Flexible Credential is an impactful step toward a versatile, frictionless payment ecosystem. It’s a promising development that aligns with consumers’ growing preference for flexibility in managing finances — an essential edge in the competitive payments industry.

Source: Visa

I highly recommend following my partner at Connecting the dots in payments... Arthur Bedel 💳 ♻️ for more great content like this one👌

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()