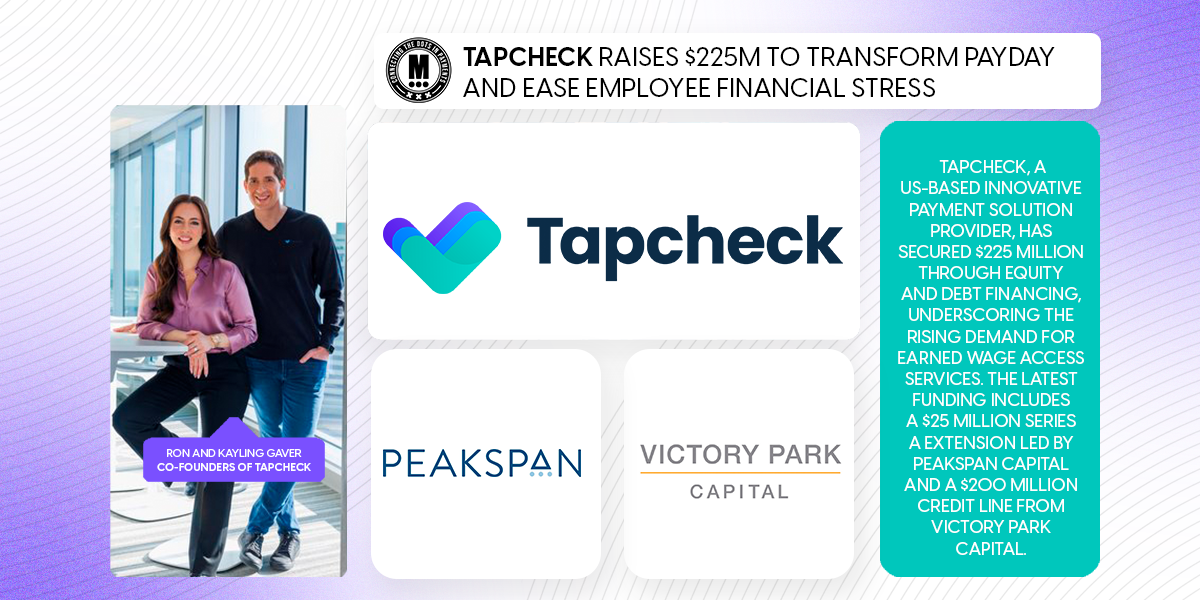

Tapcheck Raises $225M to Transform Payday and Ease Employee Financial Stress

Hey Payments Fanatic!

Tapcheck, a US-based innovative payment solution provider, has secured $225 million through equity and debt financing, underscoring the rising demand for earned wage access services. The latest funding includes a $25 million Series A extension led by PeakSpan Capital and a $200 million credit line from Victory Park Capital.

Launched in 2019 by entrepreneurial husband-and-wife team Ron and Kayling Gaver, Tapcheck enables employees to access earned wages instantly, improving cash flow and reducing financial stress without added costs for employers. Notably, companies adopting Tapcheck's solution report retention boosts exceeding 50%, with 70% of workers acknowledging significant reductions in financial anxiety.

Tapcheck has already facilitated over $1 billion in early wage distributions and partners with major brands including Hilton, Taco Bell, and Planet Fitness. The latest funding will fuel further product innovation, enhance AI-driven solutions, and expand the reach of its Mastercard-enabled service.

Amid rising demand for flexible compensation tools, this significant investment positions Tapcheck to become a dominant force in earned wage access, redefining financial wellness and workforce satisfaction for millions across the United States.

Read more global Payment industry updates below 👇 and I'll be back with more tomorrow!

Cheers,

Get the Latest in Paytech! Join my new Telegram channel for daily updates on paytech trends and exclusive insights. Connect with industry enthusiasts and stay on top of innovation!

INSIGHTS

🇨🇴 Real-time payments are reshaping financial systems worldwide. In September 2025, Colombia will join this shift with Bre-B, a new system designed to modernize digital transactions. According to ACI Worldwide’s report, “Real-time payments: Economic impact and financial inclusion,” this type of payments could bring over 5.1 million Colombians into the financial system by 2028 and boost GDP by US$282M. Read the full analysis by Sonia Gómez, ACI Director of Solution Consulting - LatAm.

PAYMENTS NEWS

🇪🇺 Ecommpay helps HiQi simplify fuel payments across Portugal and Spain. This partnership enables its customers to top up their credit account quickly and simply via their preferred payment method. The app allows private and business drivers to refuel and pay hassle-free, directly from the app.

🇪🇺 Digital assets firm Gemini allows EU traders to use Plaid to deposit funds to wallets from bank accounts, which is described as a “significant enhancement” that will allow users in the region to fund their accounts and trade crypto with ease. Continue reading

🇺🇸 FinGoal partners with unified API platform Quiltt. By integrating FinGoal’s transaction enrichment capabilities with Quiltt’s API, innovators and builders will now be able to offer their users a more insightful and personalized financial experience, across any of the open banking data access providers Quiltt supports.

🇪🇺 PayFuture granted full approval for EU EMI License. The license approval marks a major milestone in PayFuture Group’s growth strategy, enabling EU merchants to expand their global reach into emerging markets through alternative payment methods (APMs) and with future capabilities to support card payments.

🇬🇧 JP Morgan launches blockchain-based Kinexys Digital Payments in GBP / UK. As a result, it can now provide 24/7 support for corporate payments and foreign exchange for dollars, euros and pounds. The first clients to use the sterling services in London are LSEG’s SwapAgent and commodities trader Trafigura.

🇪🇺 Paysera selects iPiD as a strategical partner for VoP compliance and for global account verification. This collaboration aims to strengthen Paysera’s Know Your Payee (KYP) processes and ensure compliance with new EU regulations requiring financial institutions to verify payee details before processing transfers in euros.

🇮🇪 TransferMate promotes Product Chief Gary Conroy to CEO. Conroy will take over from Sinéad Fitzmaurice, who is stepping down after six years in the role. While Fitzmaurice will remain "involved with the business", TransferMate has not disclosed the nature of her future position.

🇦🇪 Emirates NBD launches Visa+ simplifying international money transfers. This innovative service offers Emirates NBD’s customers a more convenient, secure and faster way to send money to Visa cardholders within the GCC, reshaping the remittance and money transfer landscape in the UAE.

🇦🇪 Visa enables money transfers through BenefitPay by mobile number in Bahrain. Visa+ service allows users to send money to Visa cardholders within GCC using only the recipient's mobile number. This move marks the first step in building a broader ecosystem that aims to connect multiple banks across markets.

GOLDEN NUGGET

𝐓𝐡𝐞 𝐈𝐧𝐭𝐫𝐨𝐝𝐮𝐜𝐭𝐢𝐨𝐧 𝐭𝐨 𝐂𝐚𝐫𝐝𝐬 𝐢𝐧 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 by Travel & Payments 👇

𝐓𝐡𝐞 𝐓𝐲𝐩𝐞𝐬 𝐨𝐟 𝐂𝐚𝐫𝐝𝐬 — Edition #1

𝐔𝐧𝐝𝐞𝐫𝐬𝐭𝐚𝐧𝐝𝐢𝐧𝐠 𝐘𝐨𝐮𝐫 𝐂𝐚𝐫𝐝 𝐢𝐧 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬:

Every payment card comes with key components that define its function and issuer:

► 𝐂𝐚𝐫𝐝 𝐓𝐲𝐩𝐞 (Issuing): Defines the category (e.g. cashback, rewards).

► 𝐁𝐚𝐧𝐤 𝐈𝐝𝐞𝐧𝐭𝐢𝐟𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐍𝐮𝐦𝐛𝐞𝐫 (BIN): Identifies the issuing institution and card type.

► 𝐈𝐬𝐬𝐮𝐢𝐧𝐠 𝐁𝐚𝐧𝐤: The bank that issued the card to the cardholder (e.g. Citi, Chase).

► 𝐂𝐚𝐫𝐝 𝐍𝐞𝐭𝐰𝐨𝐫𝐤: Connects issuers and acquirers (e.g. Visa, Mastercard).

► 𝐂𝐚𝐫𝐝 𝐓𝐲𝐩𝐞 (Acquiring): Indicates how the card will be processed on the acquiring side.

𝐓𝐡𝐞 𝐓𝐲𝐩𝐞𝐬 𝐨𝐟 𝐂𝐚𝐫𝐝𝐬

1️⃣ 𝐂𝐡𝐚𝐫𝐠𝐞 Cards → Pay Later in Full (American Express Green)

2️⃣ 𝐂𝐫𝐞𝐝𝐢𝐭 Cards → Pay Later in Full/Partial (Visa Signature, Mastercard World)

3️⃣ 𝐃𝐞𝐛𝐢𝐭 Cards → Pay Now (Mastercard Debit, Visa Electron)

4️⃣ 𝐏𝐫𝐞𝐩𝐚𝐢𝐝 Cards → Pay Before (Visa Prepaid, Travel Forex cards)

𝐀𝐝𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐂𝐥𝐚𝐬𝐬𝐢𝐟𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬:

► General Purpose Payment Cards (GPPC)

► Local Payment Cards

► Virtual or One-Time Use Cards

► Corporate & Purchasing Cards

► Co-Branded & Affinity Cards

► Prepaid & Stored Value Cards

► Private Label Credit Cards

𝐎𝐩𝐞𝐧 𝐋𝐨𝐨𝐩 𝐯𝐬. 𝐂𝐥𝐨𝐬𝐞𝐝 𝐋𝐨𝐨𝐩 𝐂𝐚𝐫𝐝 𝐍𝐞𝐭𝐰𝐨𝐫𝐤𝐬

4️⃣ 𝐎𝐩𝐞𝐧 𝐋𝐨𝐨𝐩 Networks (4-Party Model)

✔ Most common in global card payments

✔ Cardholder → Issuing Bank → Card Network → Acquiring Bank → Merchant

✔ Facilitated by major networks: Visa, Mastercard

✔ Scales easily through multiple participants

✔ Examples: Visa, Mastercard, UnionPay International, GIE Cartes Bancaires

3️⃣ 𝐂𝐥𝐨𝐬𝐞𝐝 𝐋𝐨𝐨𝐩 Networks (3-Party Model)

✔ Fewer intermediaries

✔ Issuer and acquirer are often the same

✔ Direct relationships with both cardholders and merchants

✔ Easier to manage but harder to scale

✔ Examples: American Express, JCB, Diners Club International

𝐍𝐞𝐱𝐭 𝐔𝐩: 𝐓𝐡𝐞 𝐊𝐞𝐲 𝐏𝐥𝐚𝐲𝐞𝐫𝐬 𝐢𝐧 𝐂𝐚𝐫𝐝 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬

In the next edition, we’ll explore the roles of issuers, acquirers, card networks, payment gateways, and aggregators, and how they enable card transactions around the world.

Source: Travel & Payments

I highly recommend following my partner at Connecting the dots in payments... Arthur Bedel 💳 ♻️ for more great content like this one👌

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()