Rain Secures $24.5M to Scale Stablecoin Card Issuing

Hey Payments Fanatic!

Stablecoins are becoming more integrated into traditional finance, with Rain securing $24.5 million in funding to expand its stablecoin-powered card issuing platform. The round, led by Norwest Venture Partners, brings new capital to support Rain’s growing role in digital payments.

Alongside the funding, Rain announced its principal membership with Visa, expanding its issuance footprint across Europe, the U.S., and Latin America, unlocking the ability to sponsor and operate card programs in over 100 countries.

Rain operates at the core of stablecoin interoperability, allowing businesses to issue physical and virtual cards linked to self-custody wallets, custodial solutions, or traditional fiat accounts. Unlike conventional crypto-linked cards, Rain’s technology enables direct stablecoin settlement without the need for prior conversion to fiat.

“This new funding allows us to increase interoperability with existing rails, expand our footprint, and invest in our stablecoin authorization and settlement infrastructure that continues to unlock growth for our partners,” said Farooq Malik, CEO and Co-Founder of Rain.

Coincidence or not, Rain has also been linked to Worldcoin’s plans for a stablecoin payment wallet, with reports suggesting a possible role in Visa’s “mini bank account” initiative. While details remain scarce, its potential involvement in Worldcoin’s project adds another layer to the evolving stablecoin payment landscape—one worth keeping an eye on.

If you’re interested in reading a bit about what’s been happening in Payments, keep scrolling!

Cheers,

INSIGHTS

Klarna's workforce has dropped 36% since May 2022, with a steady decline existing before AI adoption. This suggests a pre-IPO slimming strategy rather than AI-driven efficiency. Employees call it "Klarnageddon," viewing it as a quiet layoff process rather than redeployment.

PAYMENTS NEWS

🇬🇧 Visa announces new change to VAMP rules: Here’s what you need to know by Solidgate. Visa updated its VAMP rules: Starting April 1, 2025, TC40 fraud alerts resolved via RDR will count toward the VAMP ratio. Fraudulent chargebacks may impact metrics, making strong fraud prevention crucial.

🇬🇧 Ecommpay shortlisted in four Retail Systems Awards. The company has been named a finalist in four categories at the 20th annual awards: Innovative Payment Solution of the Year, Payments System of the Year, Payments Innovation Award, and Fraud Prevention Solution of the Year. The ceremony will bring together the industry’s best and brightest for the biggest evening in the retail technology calendar.

🇺🇸 ACI Worldwide CEO on critical importance of payment processing & company outlook. Tom Warsop says his platform can handle “trillions of dollars” reliably every single day. His company handles things like wire transfers, debit card charges worldwide, and other similar transactions. Watch the complete interview

🇸🇬 BC Payments secures In-Principle Approval for Major Payment Institution license from MAS. The MPI license enables the company to utilize Banking Circle’s global clearing network, providing seamless cross-border payment services and acting as a key regional hub in its global payments operations.

🇺🇸 Klarna warns of internal reporting weaknesses. Klarna is preparing for a stock market listing in the U.S. In its preliminary prospectus, the firm warns about weaknesses in its internal financial reporting controls, which could potentially lead to significant errors in its financial reports.

🇺🇸 Viamericas launches cash-to-cash money transfer service for quick and easy U.S. money transfers. This new service improves how customers send and receive money within the United States, with funds available for cash pickup at any participating Viamericas location.

🇸🇦 Madfu secures Sharia certification for its BNPL solution. This certification reinforces Madfu’s commitment to providing Sharia-compliant BNPL solutions, in alignment with the Kingdom’s vision of fostering financial inclusivity through innovative FinTech services.

🇺🇸 FinTech Cross River and Forward bring payouts as a service to software developers. The collaboration empowers SaaS providers, offering them a strategic advantage in an increasingly competitive landscape and leaving a lasting impact on the financial operations of the industry.

🇬🇧 ExpenseOnDemand chooses Moneyhub to power cutting-edge Expense Management Solution. This new collaboration will help transform the way businesses handle credit card expenses by integrating intelligent Open Banking technology with a high level of customer support.

🇨🇿 Liberis and Teya team up to deliver flexible SME funding in the Czech Republic and Slovakia. Through this partnership, Liberis and Teya want to support merchants in the Czech Republic and Slovakia by bringing fast and flexible funding options tailored to their needs and demands.

🌍 Ex-Network International execs raise $6.75M for Enza, an African FinTech serving banks. The new capital will go toward expanding the team and rolling out new products for its banking clientele across Africa. Continue reading

🇮🇪 TransferMate joins RTGS.global network. TransferMate will deliver seamless, real-time international payments for RTGS.global’s business customers, reducing reliance on traditional banking intermediaries and eliminating the risk associated with moving money cross-border.

🇳🇱 Robert-Jan Lieben joins EBANX to drive European expansion. He will be based in Amsterdam, strengthening EBANX’s ties with European companies. This appointment follows other regional initiatives, including EBANX’s Payments Summit held in Barcelona, Spain, last September.

🇿🇼 Mobile-Money platform Mukuru aims to grow its African business. The platform, which was awarded a deposit-taking microfinance license by the Reserve Bank of Zimbabwe in December, has permission to operate in 50 different territories. Keep reading

🇺🇸 CLEAR partners with Stripe to power billing and payments for millions of customers. With Stripe, CLEAR is bringing a fast and easy experience to how its customers pay with Stripe’s ease of use, support for digital wallets and other payment methods, and higher conversion rates.

🇸🇦 Saudi FinTech Arabian Pay receives investment to expand BNPL offerings. The FinTech has raised an undisclosed investment as part of its Pre-Seed round from Al Bassami Holding Group. This investment will enable it to enhance its market presence, accelerate the development of its platform, and expand its partnerships.

🇫🇮 Tietoevry teams with Tapeeze on customizable payment cards. Through this partnership, they will enable banks, FinTechs, and branded organizations to create their own branded multi-function cards including flexible, secure payment functionality - without the need for complex infrastructure or regulatory approvals.

🇮🇳 Juspay open sources payment orchestrator amid FinTech industry shakeup. Juspay’s newly open-sourced orchestration technology will allow merchants to self-host the solution within their infrastructure, enabling them to integrate with a diverse range of payment providers while defining their own transaction rules.

GOLDEN NUGGET

Understanding 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 and 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐒𝐞𝐜𝐮𝐫𝐢𝐭𝐲 — by Pomelo👇

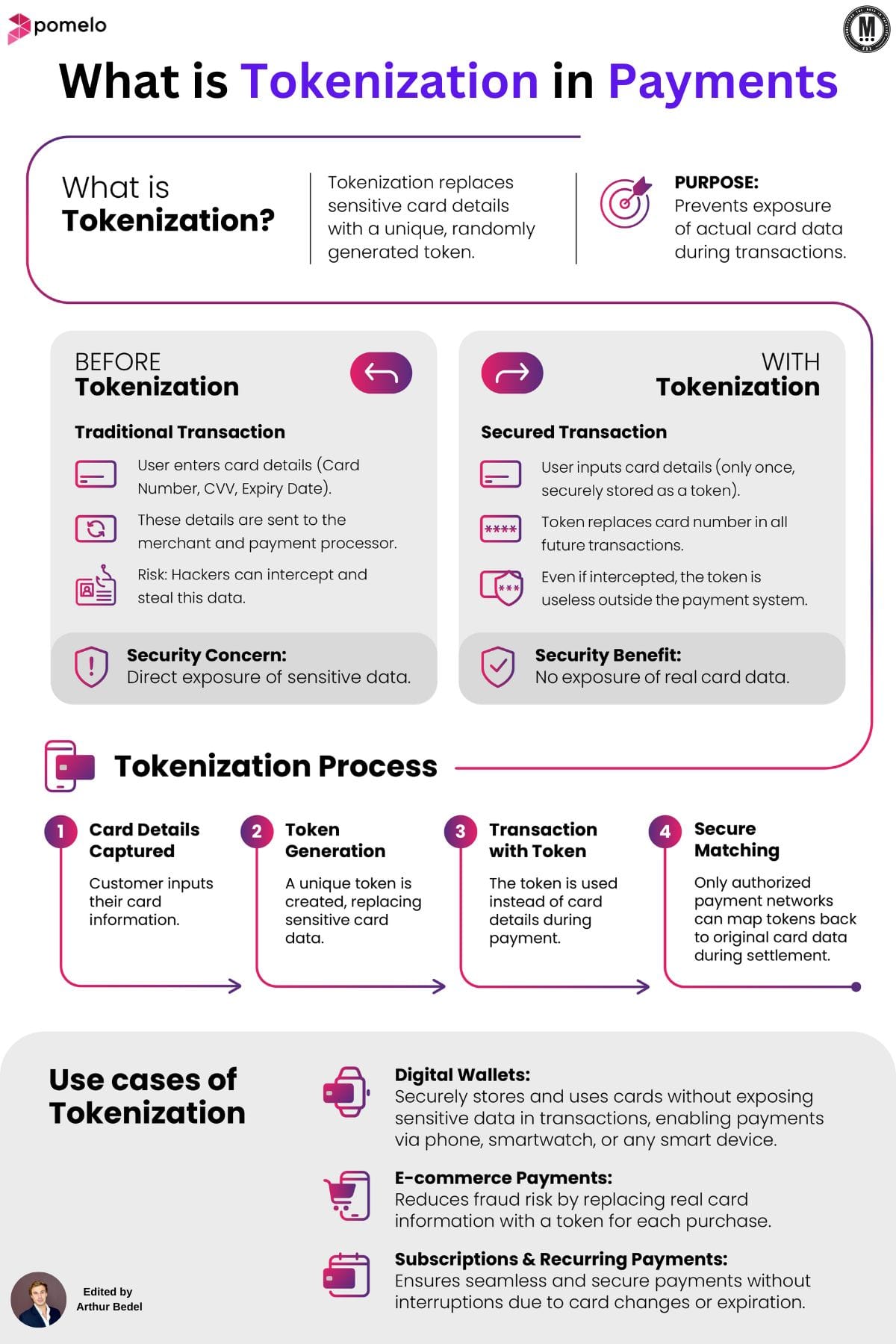

𝐃𝐞𝐟𝐢𝐧𝐢𝐭𝐢𝐨𝐧 𝐨𝐟 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐢𝐧 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬

► Tokenization replaces sensitive card details with a unique, randomly generated token, ensuring that actual card data is never exposed during transactions.

𝐏𝐮𝐫𝐩𝐨𝐬𝐞 𝐨𝐟 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧

► The main goal of Tokenization is to prevent the exposure of sensitive card details, reducing the risk of fraud and unauthorized transactions.

𝐁𝐞𝐟𝐨𝐫𝐞 𝐚𝐧𝐝 𝐖𝐢𝐭𝐡 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧

𝐁𝐞𝐟𝐨𝐫𝐞 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 (𝐓𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧𝐬)

► Users enter card details (Card Number, CVV, Expiry Date).

► These details are sent to the merchant and payment processor.

► Security Concern: Hackers can intercept and steal this data.

𝐖𝐢𝐭𝐡 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 (𝐒𝐞𝐜𝐮𝐫𝐞𝐝 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧𝐬)

► Users enter card details only once, which are securely stored as a token.

► The token replaces the card number in all future transactions.

► Even if intercepted, tokens are useless outside the payment system.

► Security Benefit — No exposure of real card data.

𝐓𝐡𝐞 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐏𝐫𝐨𝐜𝐞𝐬𝐬

1️⃣ 𝐂𝐚𝐫𝐝 𝐃𝐞𝐭𝐚𝐢𝐥𝐬 𝐂𝐚𝐩𝐭𝐮𝐫𝐞𝐝

► The customer inputs their card information at checkout.

2️⃣ 𝐓𝐨𝐤𝐞𝐧 𝐆𝐞𝐧𝐞𝐫𝐚𝐭𝐢𝐨𝐧

► A unique token is created, replacing sensitive card data. There are several type of tokens — Merchant, PSP, Network Tokens etc...

3️⃣ 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧 𝐰𝐢𝐭𝐡 𝐓𝐨𝐤𝐞𝐧

► The token is used instead of card details during payment.

4️⃣ 𝐒𝐞𝐜𝐮𝐫𝐞 𝐌𝐚𝐭𝐜𝐡𝐢𝐧𝐠

► Only authorized payment networks can map tokens back to the original card during settlement.

𝐔𝐬𝐞 𝐂𝐚𝐬𝐞𝐬 𝐨𝐟 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧

► 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐖𝐚𝐥𝐥𝐞𝐭𝐬 – Securely store and use cards without exposing sensitive data when making payments via phone, smartwatch, or any smart device.

► 𝐄-𝐜𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 – Reduces fraud risk by replacing real card details with a token for each transaction.

► 𝐒𝐮𝐛𝐬𝐜𝐫𝐢𝐩𝐭𝐢𝐨𝐧𝐬 & 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 – Ensures seamless and secure payments, preventing service interruptions due to card expiration or changes.

Source: Pomelo

I highly recommend following my partner at Connecting the dots in payments... Arthur Bedel 💳 ♻️ for more great content like this one👌

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()