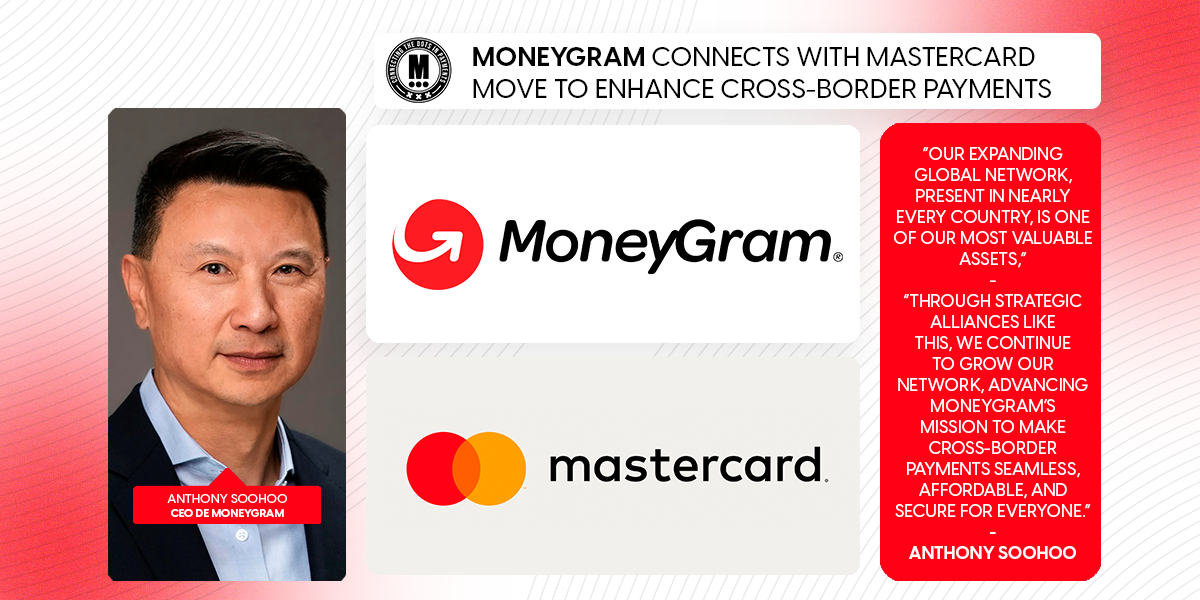

MoneyGram Connects with Mastercard Move to Enhance Cross-Border Payments

Hey Payments Fanatic!

Only those who have dealt with it know the frustration of sending money abroad. Mastercard and MoneyGram are teaming up to change that.

By integrating Mastercard Move into its network, MoneyGram will make global money transfers faster, more secure, and more accessible. U.S. customers can now send funds to 38 countries using any U.S.-issued Mastercard card. The initiative also connects users to nearly 10 billion endpoints worldwide, simplifying cross-border payments. Additional enhancements are expected throughout 2025.

“Our expanding global network, present in nearly every country, is one of our most valuable assets,” said Anthony Soohoo, CEO of MoneyGram. “Through strategic alliances like this, we continue to grow our network, advancing MoneyGram’s mission to make cross-border payments seamless, affordable, and secure for everyone.”

The impact will be clear: faster transfers, lower costs, and greater financial access. Customers can send funds to bank accounts, mobile wallets, and cash pick-up locations, all with the reliability of Mastercard’s trusted infrastructure.

“By integrating Mastercard Move into MoneyGram’s vast network, we’re building in speed and added peace of mind into every transaction so that critical funds can get into hands when and where it’s needed,” said Chiro Aikat, U.S. Co-President, Mastercard.

If you want to catch up on the latest in Payments, keep scrolling!

Cheers,

INSIGHTS

🇮🇳 Only 4% of all payment transactions move half of India's money.

PAYMENTS NEWS

🇸🇪 Mollie launched in Sweden. Mollie is now available for Swedish businesses and is already helping many customers accelerate their sales, reduce costs, and save time with solutions that simplify every payment process. This expansion represents another important step towards achieving the goal of expanding into new markets.

🇬🇧 Ecommpay named as one of the Payments Power 50. Inaugural power list recognises the inclusivity and sustainability credentials of payment platform helping businesses increase financial inclusion. Ecommpay’s commitment to Equality, Diversity and Inclusion (EDI) does not just meet regulatory expectations; it goes further, to build trust and strengthen brand reputation and customer loyalty.

🇬🇧 Solidgate launches Verifi-Powered API for streamlined chargeback management. This collaboration aims to make dispute resolution faster and easier for merchants. With Verifi’s new infrastructure, RDR API enables merchants to instantly accept or decline disputes as they are submitted to Visa by card issuers.

🇲🇽 DEUNA’s new express flow powered by PayPal Vaulting. The integration enables businesses to securely store PayPal credentials and offer a seamless checkout experience. This innovative solution enhances the checkout experience for PayPal users by eliminating unnecessary friction.

🌎 CellPoint Digital partners with Kushki to bring seamless, intelligent payments to Latin America. By combining Kushki’s local acquiring power with CellPoint Digital’s orchestration and optimization expertise, they are enabling merchants to simplify their payment setup, unlock new markets, and enhance the customer experience, all through a single connection.

🇺🇸 Mastercard expands crypto capabilities with new services for digital asset users. These initiatives include the expansion of the Mastercard Crypto Credential and the development of a Multi-Token Network (MTN), marking a significant push into blockchain-based financial solutions.

🇵🇱 Visa and ZEN.COM team up on real-time cross-border payments through Visa Direct. By leveraging Visa Direct, ZEN will be able to offer its customers a seamless and reliable cross-border payment experience. Keep reading

🇩🇰 Lunar partners with SAS - Scandinavian Airlines, to give the SAS EuroBonus Lunar card a little upgrade. The SAS x Lunar card is a co-branded debit card that allows users to turn their everyday spending into EuroBonus points. Given the high value users place on it, the benefits are now being further enhanced.

🇬🇧 Thredd appoints Simeon Lando as Chief Marketing Officer. With over 25 years of experience in B2B marketing, Lando has led enterprise technology and payments-focused marketing teams at leading companies. His expertise in developing and implementing client-centric marketing strategies will be instrumental in supporting Thredd’s next phase of growth.

🇬🇧 PayPal announces Ads Solution in the UK, revolutionising commerce media for brands and merchants. The solution enables interested PayPal users to discover relevant brands and products that enhance their shopping experience while also helping merchants grow their business.

🇬🇧 Wincent selects OpenPayd to power its global payment operations. Through this partnership, Wincent will leverage OpenPayd’s robust global banking and real-time payment network to deliver enhanced fiat capabilities for its institutional client base.

🇰🇪 Visa appoints John Njoroge as new Country Manager for Kenya South Sudan & Somalia. In this role, John will drive Visa’s strategic growth, enhance client relationships, and spearhead the expansion of digital payment solutions across the three markets.

🇺🇸 Visa bids $100m to replace Mastercard as Apple’s new credit card partner. Visa has made a bold push to secure the Apple Card, offering an upfront payment typically reserved for the largest card programs. Read more

🇳🇿 Laybuy returns, powered by Klarna, combining a trusted Kiwi brand with Klarna’s global expertise. With 93M+ active users and 675K retailers in 26 markets, Klarna enhances Laybuy to make shopping smarter and safer for Kiwi consumers while driving merchant growth.

🇬🇧 Eurostar introduces Klarna for flexible payments in the UK and France. Customers checking out on Eurostar.com can now choose Klarna’s Pay in 3, allowing them to split the cost of their ticket into three equal, interest-free payments, or Pay in Full for a seamless one-time transaction.

🇱🇹 myTU introduces Google Pay for secure contactless payments. This new feature enables individuals and businesses to add their debit cards to Google Wallet, making payments more convenient and secure. myTU’s customers can now pay in stores, apps, or online with just their smartphones or other Android devices.

🇺🇸 Stablecoin issuer Circle files publicly for IPO as revenue grows. The company reported a net income of $156 million on a revenue of $1.68 billion in 2024, compared with a net income of $268 million on $1.45 billion in revenue the previous year.

🇮🇳 Paytm partners with Hyderabad civic body to digitize property tax collection. The fintech firm has deployed over 400 Paytm All-In-One EDC devices (card machines) across collection centers and for door-to-door tax payments. These machines allow residents to pay property tax using credit cards, debit cards, and QR codes.

GOLDEN NUGGET

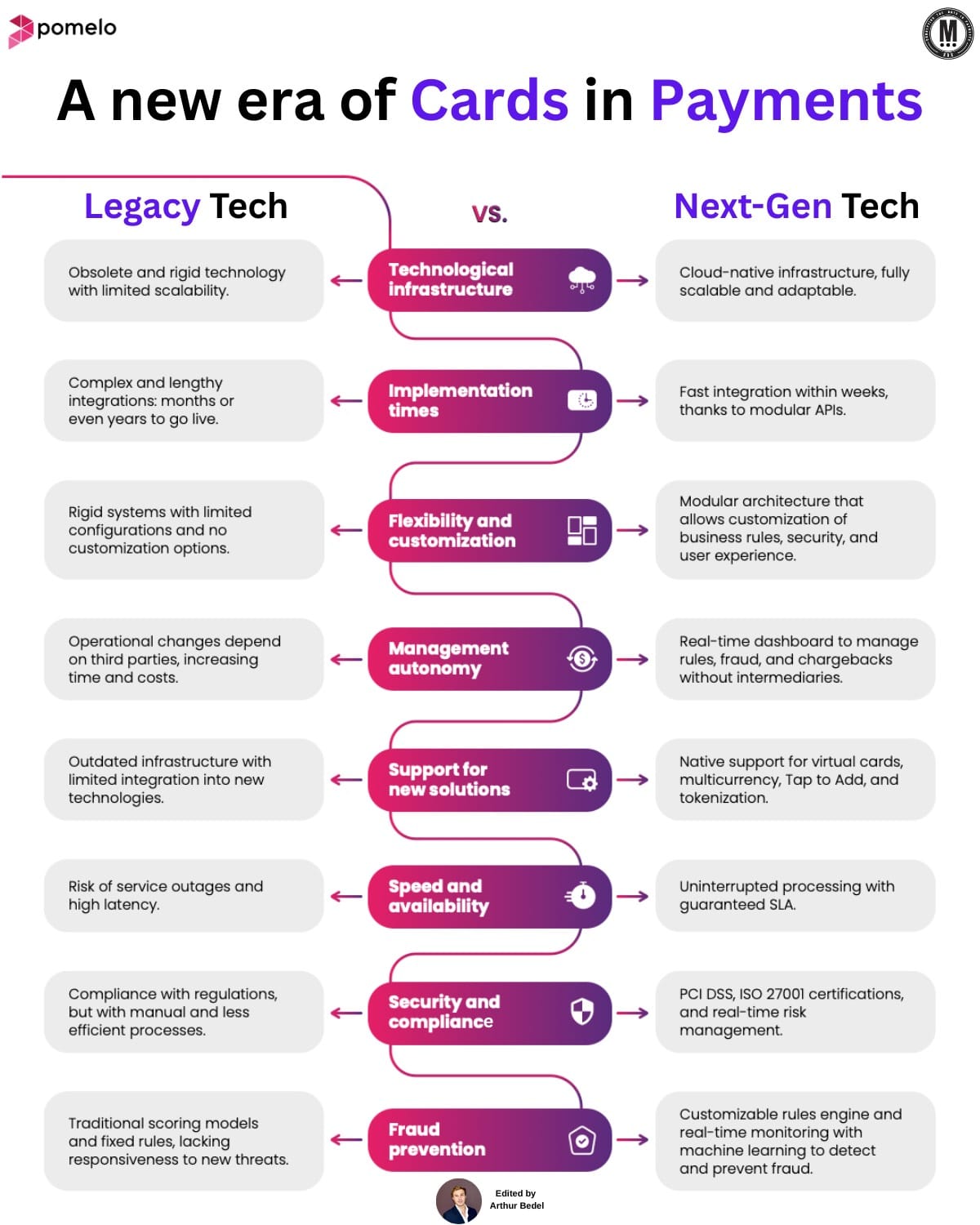

𝐋𝐞𝐠𝐚𝐜𝐲 vs 𝐍𝐞𝐱𝐭-𝐆𝐞𝐧 𝐂𝐚𝐫𝐝 𝐈𝐬𝐬𝐮𝐢𝐧𝐠 by Pomelo — a new era of cards👇

► 𝐋𝐞𝐠𝐚𝐜𝐲 𝐂𝐚𝐫𝐝 𝐈𝐬𝐬𝐮𝐢𝐧𝐠 relied on singular, rigid systems with limited scalability, lengthy integrations, and minimal flexibility. These systems required third-party management for changes, leaving businesses with slow implementations and increased costs.

Examples → TSYS, FIS, Fiserv

► 𝐍𝐞𝐱𝐭-𝐆𝐞𝐧 𝐂𝐚𝐫𝐝 𝐈𝐬𝐬𝐮𝐢𝐧𝐠 introduces cloud-native, API-driven platforms that enable rapid program launches, real-time decision-making, and seamless product expansion. This modern approach eliminates traditional bottlenecks, allowing faster growth, improved security, and scalability.

Examples → Pomelo, Marqeta, Galileo Financial Technologies

𝐋𝐞𝐠𝐚𝐜𝐲 𝐯𝐬. 𝐍𝐞𝐱𝐭-𝐆𝐞𝐧 𝐈𝐬𝐬𝐮𝐢𝐧𝐠 𝐒𝐭𝐚𝐜𝐤 👇

1️⃣ Technological Infrastructure

► Legacy: Obsolete, rigid technology with limited scalability.

► Next-Gen: Cloud-native, API-driven, scalable, and adaptable infrastructure.

2️⃣ Implementation Times

► Legacy: Complex and lengthy integrations, taking months or years.

► Next-Gen: Fast integration within weeks, leveraging modular APIs.

3️⃣ Flexibility & Customization

► Legacy: Rigid systems with limited configurations and no flexibility.

► Next-Gen: Modular architecture that customizes business rules, security, and user experiences.

4️⃣ Management Autonomy

► Legacy: Operational changes rely on third parties, increasing time and costs.

► Next-Gen: Real-time dashboards allow rule management, fraud monitoring, and chargeback handling without intermediaries.

5️⃣ Support for New Solution

► Legacy: Limited integration into new technologies.

► Next-Gen: Native support for virtual cards, multicurrency, Tap to Add, and tokenization.

6️⃣ Speed & Availability

► Legacy: Prone to service outages and high latency.

► Next-Gen: Uninterrupted processing with guaranteed SLA and high availability.

7️⃣ Security & Compliance

► Legacy: Manual compliance with regulations that is less efficient.

► Next-Gen: Compliance with PCI DSS, ISO 27001 certifications, and real-time risk management.

8️⃣ Fraud Prevention

► Legacy: Traditional scoring models with fixed rules that lack responsiveness to new threats.

► Next-Gen: Real-time monitoring and customizable rules powered by machine learning to detect and prevent fraud.

Pomelo 𝐔𝐬𝐞 𝐂𝐚𝐬𝐞:

✅ Unprecedented Speed → Launch multiple programs in less than a month, tailored to each business.

✅ Record-breaking Tokenization → Implemented in under 18 days with just two APIs.

✅ Limitless Issuance → Over 260 cards per second without compromising performance.

✅ Seamless Expansion → Expand products and markets with a single integration.

✅ Real-Time Decisions → Operate autonomously with a live dashboard for frictionless decisions.

Source: Pomelo

I highly recommend following my partner at Connecting the dots in payments... Arthur Bedel 💳 ♻️ for more great content like this one👌

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()