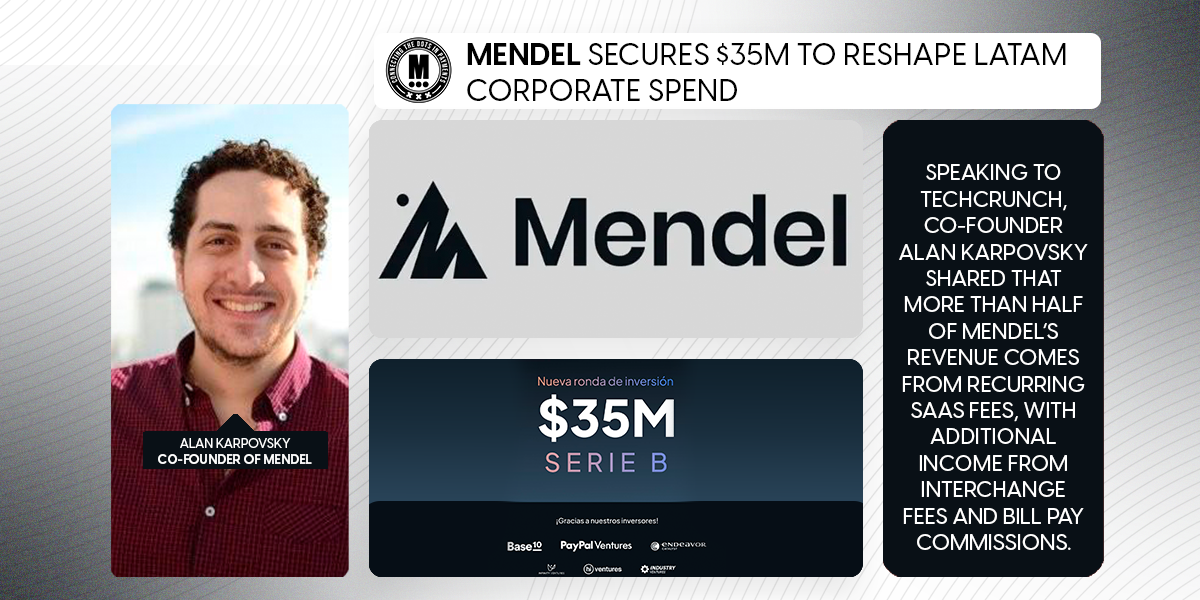

Mendel Secures $35M to Reshape LatAm Corporate Spend

Hey Payments Fanatic!

Mendel, a Mexico-based FinTech working to simplify corporate expenses in Latin America, has just raised $35 million in a Series B round, bringing its total funding to $60 million. This fresh capital will help expand its offerings and support its entry into new markets.

The round was led by Base10 Partners, with new investors PayPal Ventures and Endeavor Catalyst joining existing backers like Infinity Ventures, Industry Ventures, and Hi.vc.

Founded in 2021, Mendel provides an integrated platform that combines expense management, payments, and corporate travel. Unlike many global competitors, it focuses on the complexities of Latin America’s regulatory landscape, tackling tax codes, invoicing requirements, and multi-currency workflows.

Speaking to TechCrunch, co-founder Alan Karpovsky shared that more than half of Mendel’s revenue comes from recurring SaaS fees, with additional income from interchange fees and bill pay commissions.

The company has reported a 2.5x year-over-year growth in ARR, with gross margins exceeding 75%. It currently serves around 500 customers, including Mercado Libre, FEMSA, Adecco, and McDonald’s. While not yet profitable, Mendel expects to reach that milestone by late 2025.

With this latest round, the company is gearing up for expansion beyond Mexico and Argentina. Plans are in motion to enter Chile, Colombia, and Peru in 2025, with Brazil set to follow in 2026.

If you want to catch up on the latest in Payments, keep scrolling!

Cheers,

INSIGHTS

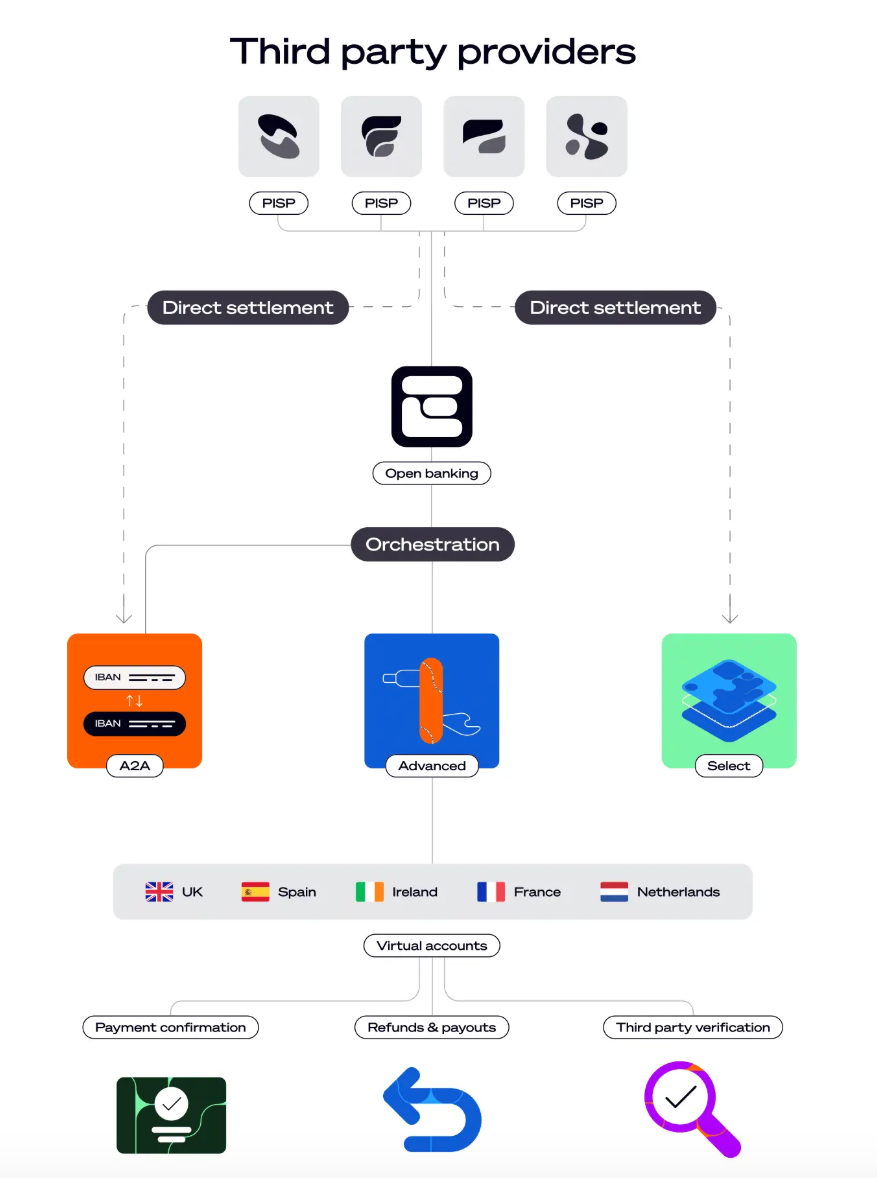

How to drive more conversions with open banking solutions by Ecommpay. This article explores how open banking streamlines payments, reduces cart abandonment, and increase sales by enabling instant, user-friendly transactions. Discover more in the full article—click here

PAYMENTS NEWS

🇬🇧 Interflora achieves highest ever acceptance rate of 95.4% with Checkout.com ahead of Mother’s Day surge. Checkout.com enables Interflora’s customers to pay with ease using Apple Pay and Google Pay, which now account for 20% of mobile transactions. These mobile-friendly options are critical during high-pressure gifting occasions, where speed and convenience drive conversion.

🇨🇴 FinTech firm Monet and Refácil launch solution for paying bills on credit in Colombia. This new service will allow users to pay household bills such as water, electricity, gas, phone, and television, without the need to have cash at the time of the transaction.

🇦🇪 UAE set to launch Digital Dirham CBDC this year. This will be accepted across all payment channels alongside physical currency and accessible through licensed financial institutions. It will feature high security, tokenization, and smart contract integration, enabling instant settlements and multi-party transactions.

🇨🇴 Transfiya, an instant payment system, has 99.99% availability in Colombia. The service, managed by ACH Colombia, handled 300 million transactions in 2024 and serves over 22 million users, providing fast, secure, and efficient money transfers across different financial institutions.

🌎 QorPay integrates with Visa’s Cybersource to support secure payments. By leveraging Visa’s technology, QorPay enables clients to simplify transactions, mitigate fraud risks, orchestrate data, and optimise expense management through a unified dashboard.

🇬🇧 Zempler partners with Wise to roll out international payment service. The initial launch of the service will allow users to send payments in US dollars and euros and will be available for accounts in the Single Euro Payment Area (SEPA) region.

🇮🇳 Axis Bank launches 24/7 global USD clearing through Kinexys by J.P. Morgan. This collaboration will enable Axis' commercial clients to make cross-border payments anytime, streamlining payments and unlocking liquidity through blockchain technology, boosting the bank's position in the international banking sector.

🇺🇸 NMI launches Tap To Pay on Google Play Store. NMI’s Tap to Pay solution gives its partners a simple way to help merchants and small businesses accept payments on the Android smartphones or tablets they already use, eliminating the expense and complexity of deploying traditional point-of-sale equipment.

🇺🇸 CFPB set to ditch BNPL rule. The rule would have required BNPL providers to grant consumers key legal protections and rights similar to those of conventional credit cards. These include the right to dispute charges and request a refund from the lender after returning a product purchased with a buy now, pay later loan.

GOLDEN NUGGET

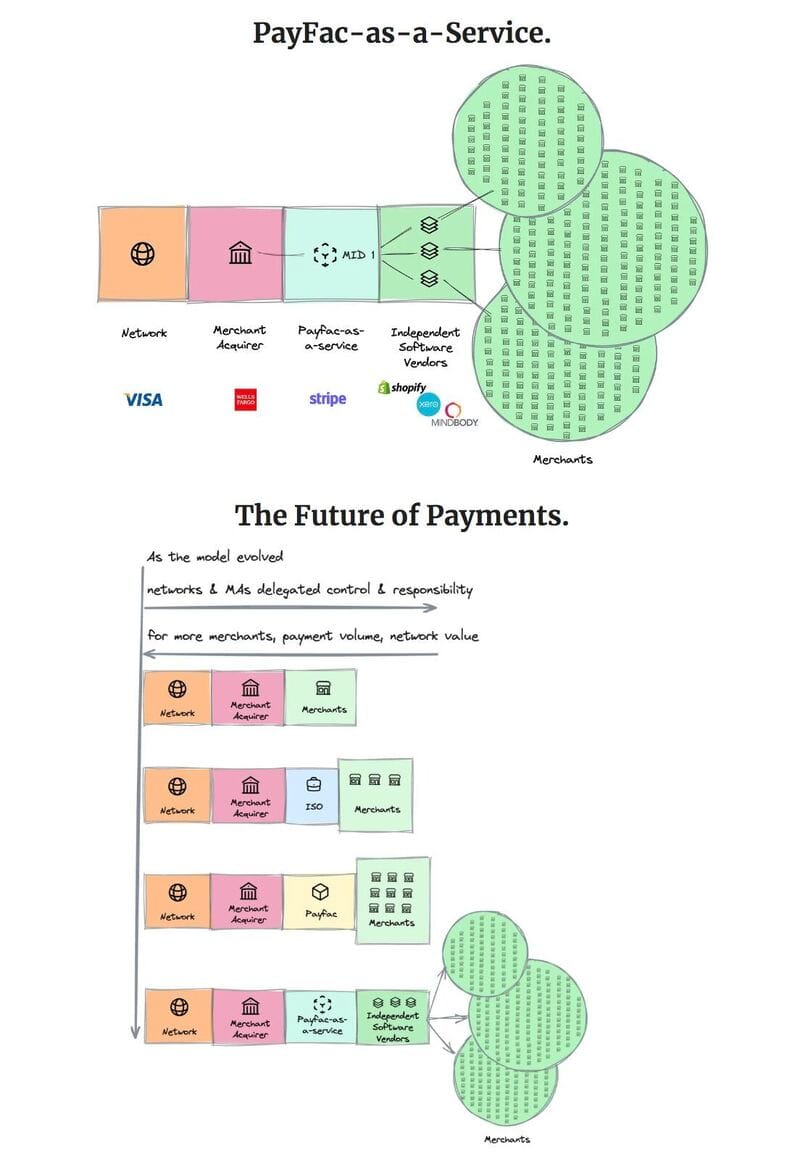

𝗣𝗮𝘆𝗳𝗮𝗰 is the model behind FinTech’s biggest successes, from Stripe and Square to Shopify, Uber, and more. It's a critical but often misunderstood topic, so let's break it down:

The Payfac model, pivotal to FinTech giants like Stripe and Square, streamlines the traditional, cumbersome process of card payments, transforming how money moves between parties.

It originated as a response to the costly and complex setup of merchant acquirers (MAs) and independent sales organizations (ISOs), which provided card payment services to merchants but often excluded smaller, riskier vendors due to high costs.

Innovations in mobile and cloud computing around 2008, exemplified by companies like Square and Stripe, introduced payment facilitators (payfacs) that aggregated merchants under shared merchant IDs, simplifying the onboarding process and expanding market access.

This evolution spurred the development of Payfac-as-a-Service (PFaaS), enabling platforms like Shopify to offer payment services through partnerships with payfacs, thereby leveraging network effects to enhance the value of payment networks.

This shift underscores the ongoing transformation in financial services, driven by software innovation that lowers barriers to entry, expands services, and fosters a more interconnected market landscape.

I highly recommend reading another masterpiece blog post by Matt Brown called “Payfac in 1,000 words” for a deeper dive into this topic.

The future of Payments, according to Matt:

“The payfac and PFaaS trends exemplify the effect of software on financial services and other industries: it lowers fixed costs and enables new distribution channels, pushing the service closer to the end user in a more integrated, user-friendly, and cost-effective way.

These trends also reiterate how much payments is fundamentally a network effect business. More acceptance = more cardholders = more payment volume = more network value.

The broader trend from ISOs to payfacs to PFaaS is one of networks and MAs delegating control and responsibility in exchange for more merchants, more payment volume, and a more valuable network.”

Source: Matt Brown

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()