Klarna Rolls Out as Default for Nexi Merchants

Hey Payments Fanatic!

Klarna and Nexi are strengthening their collaboration, bringing Klarna’s payment options to all Nexi merchants worldwide—both online and in-store. This move means small and medium-sized businesses will automatically have Klarna enabled at checkout, simplifying access to flexible payment solutions for millions of shoppers.

The rollout follows a successful pilot in the Nordics, where Nexi merchants reported higher conversion rates after integrating Klarna into their checkout process.

Nexi, a major player in European PayTech, operates across 25+ countries, serving banks, merchants, and consumers with seamless payment solutions. Klarna, known for its flexible payment options, will now be the default in Nexi’s checkout, helping merchants attract more shoppers and increase revenue.

The expansion will be particularly relevant in key markets such as Poland and Italy, where demand for alternative payment methods is rising.

If you’re curious about the latest happenings in Payments, keep reading!

Cheers,

PAYMENTS NEWS

🇨🇳 Vistra collaborates with Airwallex to empower global borderless business. This strategic partnership sees Vistra integrating Airwallex’s Business Account and Embedded Finance products into its platform, providing clients with unparalleled convenience and efficiency in managing their global operations.

🇮🇳 Google Pay adds convenience fee for bill payments in India. Google Pay’s move aligns with its competitors, which already impose processing fees for card payments on bill transactions and recharges. These fees are a response to the rising costs FinTech firms incur when processing transactions on UPI.

🇬🇧 Dodo Payments raises $1.1 million pre-seed funding. The company plans to use the funds to strengthen its technological infrastructure by introducing modules for subscriptions, billing, fraud detection, and risk management. It also aims to establish local payment rails in over 30 countries.

🇬🇧 Kani Payments secures Investment from Maven Capital Partners. The combined investment will be used to further develop Kani’s highly scalable platform, grow its team, and support international expansion with increasing digitisation in financial services, alongside greater global safeguarding regulations.

🇨🇳 American Express joins Alipay digital payment system in China. The initiative not only simplifies transactions for travellers but also provides local businesses with greater opportunities to attract international customers, the companies said.

🇪🇺 Is Wero an ‘existential threat’ to Europe’s payments startups? Backed by a consortium of 14 banks under the European Payments Initiative (EPI), France and Belgium, Wero is a digital wallet enabling consumer peer-to-peer transfers in under ten seconds.

🇺🇸 PayPal’s growth plan for earnings, Venmo expansion and new Merchant Platform. PayPal forecasts adjusted earnings per share to grow in the low teens by 2027 and 20% over the long term as it streamlines operations. A key part of this strategy is Venmo’s expansion, with CEO Alex Chriss aiming for the platform to hit $2 billion in revenue by 2027. To support businesses, the payments company has introduced PayPal Open, a unified platform that simplifies access to its merchant services.

🌎 PayPal is expanding its partnerships to enhance digital commerce globally. In the UK and Europe, it is working with J.P. Morgan Payments to scale Fastlane and strengthen merchant acquiring. Meanwhile, in the U.S., it has teamed up with Verifone to create an omnichannel platform that streamlines checkout for large retailers, restaurants, and global merchants by integrating data, security, and processing across online and in-store sales.

🇸🇦 Telr partners with Bank AlJazira to enhance digital payments in Saudi. This collaboration aims to support the country’s transition towards a cashless economy by improving transaction efficiency, security, and accessibility. Businesses can access payment links, recurring payments, e-invoicing, and BNPL.

🇰🇷 Naver Pay, Kakao Pay, and Toss Pay expand overseas payments. Korean major mobile app payment providers have scrambled to enter global markets as they face increasingly fierce competition from credit card companies in domestic markets.

🇦🇪 Stablecoin payments at POS terminals coming to UAE via AFS and Ternoa. As part of the partnership arrangement, Ternoa will introduce Athar, a decentralized consumer finance protocol. Athar makes cryptocurrency payments easier and more accessible for everyday transactions.

GOLDEN NUGGET

Welcome back to 𝐓𝐡𝐞 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐀𝐜𝐚𝐝𝐞𝐦𝐲 by Checkout.com — Episode 3👇

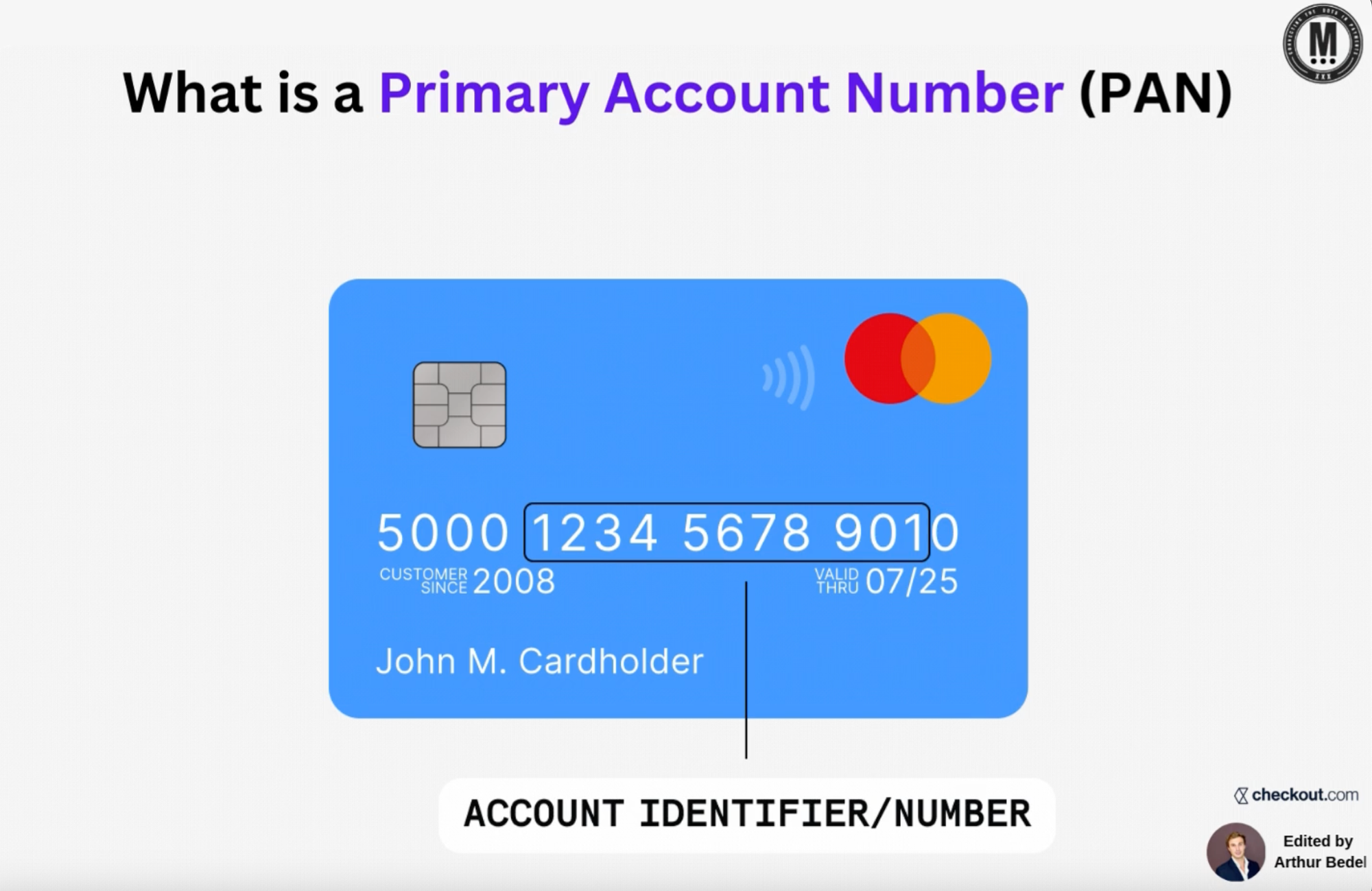

Topic #3: 𝐖𝐡𝐚𝐭 𝐢𝐬 𝐚 𝐏𝐫𝐢𝐦𝐚𝐫𝐲 𝐀𝐜𝐜𝐨𝐮𝐧𝐭 𝐍𝐮𝐦𝐛𝐞𝐫 (#PAN)

► A 𝐏𝐫𝐢𝐦𝐚𝐫𝐲 𝐀𝐜𝐜𝐨𝐮𝐧𝐭 𝐍𝐮𝐦𝐛𝐞𝐫 (PAN) is a unique identifier found on payment cards (credit, debit, and prepaid). It links the cardholder to their financial institution, enabling transactions and account management.

𝐒𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐨𝐟 𝐏𝐀𝐍:

PANs are standardized under ISO/IEC 7812, ensuring consistency across payment networks worldwide.

► 𝐌𝐚𝐣𝐨𝐫 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐈𝐝𝐞𝐧𝐭𝐢𝐟𝐢𝐞𝐫 (MII): The first digit identifies the card’s scheme, such as Visa, Mastercard, American Express, or Discover Financial Services.

► 𝐈𝐬𝐬𝐮𝐞𝐫 𝐈𝐝𝐞𝐧𝐭𝐢𝐟𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐍𝐮𝐦𝐛𝐞𝐫 (IIN)/Bank Identification Number (BIN): The first eight digits identify the institution that issued the card (Chase, HSBC...). This helps the payment system route the transaction to the correct issuer.

► 𝐀𝐜𝐜𝐨𝐮𝐧𝐭 𝐈𝐝𝐞𝐧𝐭𝐢𝐟𝐢𝐞𝐫/𝐍𝐮𝐦𝐛𝐞𝐫: The remaining digits (typically digits 5 to 16 in a 16-digit PAN) uniquely link the card to the cardholder’s specific account.

► 𝐕𝐚𝐥𝐢𝐝𝐚𝐭𝐨𝐫 𝐃𝐢𝐠𝐢𝐭 (Check Digit): The last digit is calculated using the Luhn algorithm to verify the accuracy of the entire PAN, protecting against input errors or fraud.

► 𝐒𝐞𝐜𝐮𝐫𝐢𝐭𝐲 𝐈𝐦𝐩𝐨𝐫𝐭𝐚𝐧𝐜𝐞: PANs are highly sensitive data, often tokenized or encrypted to protect against unauthorized access. Tokenization replaces the PAN with a unique identifier, enhancing payment security.

► 𝐇𝐨𝐰 𝐝𝐨 𝐭𝐡𝐞𝐲 𝐟𝐚𝐜𝐢𝐥𝐢𝐭𝐚𝐭𝐞 𝐝𝐞𝐛𝐢𝐭 𝐚𝐧𝐝 𝐜𝐫𝐞𝐝𝐢𝐭 𝐜𝐚𝐫𝐝 𝐭𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧𝐬?

1️⃣ 𝐂𝐮𝐬𝐭𝐨𝐦𝐞𝐫 𝐈𝐧𝐢𝐭𝐢𝐚𝐭𝐞𝐬 𝐏𝐚𝐲𝐦𝐞𝐧𝐭 — In a card-present transaction, the PAN is collected through the card's EMV chip, magnetic stripe, or NFC technology during contactless payments.

2️⃣ 𝐏𝐚𝐲𝐦𝐞𝐧𝐭 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 — The PAN is replaced with a token to protect sensitive data. This prevents exposure of the real PAN if security is compromised.

3️⃣ 𝐏𝐚𝐲𝐦𝐞𝐧𝐭 𝐒𝐮𝐛𝐦𝐢𝐬𝐬𝐢𝐨𝐧 — The token, transaction amount, and business details are sent to the acquiring bank.

4️⃣ 𝐈𝐬𝐬𝐮𝐞𝐫 𝐕𝐚𝐥𝐢𝐝𝐚𝐭𝐢𝐨𝐧 — The Issuer uses the PAN to locate the account, verify its validity, check for fraud, and confirm sufficient funds.

5️⃣ 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧 𝐂𝐨𝐦𝐩𝐥𝐞𝐭𝐢𝐨𝐧 — If approved, the issuing bank relays the approval through the payment network back to the acquiring bank, and finally to the point of sale, completing the transaction.

𝐓𝐡𝐞 𝐁𝐞𝐧𝐞𝐟𝐢𝐭𝐬:

✅ Security — PANs use the Luhn algorithm for fraud prevention and are often tokenized.

✅ Interoperability — Used for physical, online, and mobile transactions.

✅ Global Compatibility — Recognized and accepted by all—

Source: Checkout.com x Connecting the dots in payments...

I highly recommend following my partner Arthur Bedel 💳 ♻️ for more great content like this one👌

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()