Brazil's Instant Payments Double on Black Friday

Hey Payments Fanatic!

Brazil's instant payment system Pix has recorded a 120.7% increase in transaction value during Black Friday 2024, reaching 130 billion reais ($21.60 billion) compared to 58.9 billion reais in the previous year, according to central bank data. The system also achieved a new single-day record with 239.9 million transactions, up from 136.3 million in 2023.

Pix, launched by Brazil's central bank four years ago, has now surpassed the combined volume of credit and debit card transactions in the country. The Black Friday surge coincided with the distribution of Brazil's annual "13th salary" bonus payment to formal workers, adding to the transaction volumes.

The payment system's Black Friday performance comes amid strong household consumption in Brazil, where the unemployment rate has reached its lowest level on record. The central bank data shows Pix's growing adoption for both person-to-person and person-to-business transactions.

What are your thoughts on the rapid adoption of instant payment systems like Pix? Share your thoughts in the comments below!

It's a jam-packed newsletter full of interesting Payments News updates today, so you better get to it 👇

Cheers,

Stay Updated on the Go. Join my new Telegram channel for daily updates and real-time breaking news. Stay informed and connect with industry enthusiasts —subscribe now!

INSIGHTS

📊 The 2025 SEPA Instant Credit Transfer (SCT Inst) Rulebook by the European Payments Council (EPC) 👇

PAYMENTS NEWS

🇧🇷 PayRetailers launches enhanced solution to help betting operators comply with Brazil's new sports betting regulations.

Juan Pablo Jutgla, CEO at PayRetailers, said: “The sports betting industry in Brazil is poised for significant growth, but operators will face increasing pressure to comply with the new regulations. Our enhanced Pix solution helps operators strike the right balance between ensuring compliance while maintaining an optimal user experience.”

Daniel Niezgoda, CTO at PayRetailers, added: “As Pix becomes central to Brazil’s financial system, the need for seamless payment processing paired with compliance automation has never been greater. Our enhanced Pix solution offers real-time account validation and intelligent routing, streamlining operations while reducing risks and ensuring efficiency.”

Aeon debuts authorization payments on the TON blockchain. Users start by choosing a service or product and initiating a transaction. From there, Aeon’s system prompts them to authorize a payment, locking in the required amount, according to a press release.

🇪🇺 ECB publishes second progress report on digital euro. Since the first progress report, the ECB has updated its digital euro rulebook to harmonize payments across the euro area and concluded a call for applications to select providers of digital euro components and services.

🇨🇮 HUB2 banks $8.5M to become the ‘Stripe for Francophone Africa.’ HUB2 already works with some 55 neobanks, payment companies, remittance companies and cryptocurrency providers, and it has now picked up $8.5 million to expand that list, and to up its game in its tech stack.

🇬🇧 Nationwide partners with Experian to digitise payslip income. Nationwide will use Experian’s work report income and employment verification service, which will digitally confirm homebuyers’ declared income “removing the need for applicants to provide manual income proofs, such as copies of their payslips”.

🇺🇸 Coinbase now lets you buy crypto with Apple Pay in third-party apps. Coinbase announced an integration with Apple Pay on Monday, allowing app makers to build the ability to buy crypto with Apple Pay directly into their apps. The integration is part of Coinbase Onramp, which gives app makers a way for customers to turn their traditional currencies, such as USD, into cryptocurrencies.

🇮🇹 Construction accident triggers $106 Million Italian payments outage. Italy has restored a payment services outage that disrupted Black Friday sales on Nov. 28-29, reportedly caused by gas roadwork damaging Worldline’s network connection. Nexi was also affected and is investigating, according to Bloomberg and Reuters.

➡️ You've probably seen the Stripe BF/CM monitor. But did you know it's a real machine? 🤯 Click here for mind-blowing Stripe stats from the weekend and an insightful video!

🇰🇷 TNG eWallet Now Accepted in Korea. This partnership makes TNG eWallet the first Malaysian e-wallet endorsed by KTO, granting users access to 1.9 million ZeroPay merchants across major cities and tourist hotspots and over 3 million Visa merchants across the country.

GOLDEN NUGGET

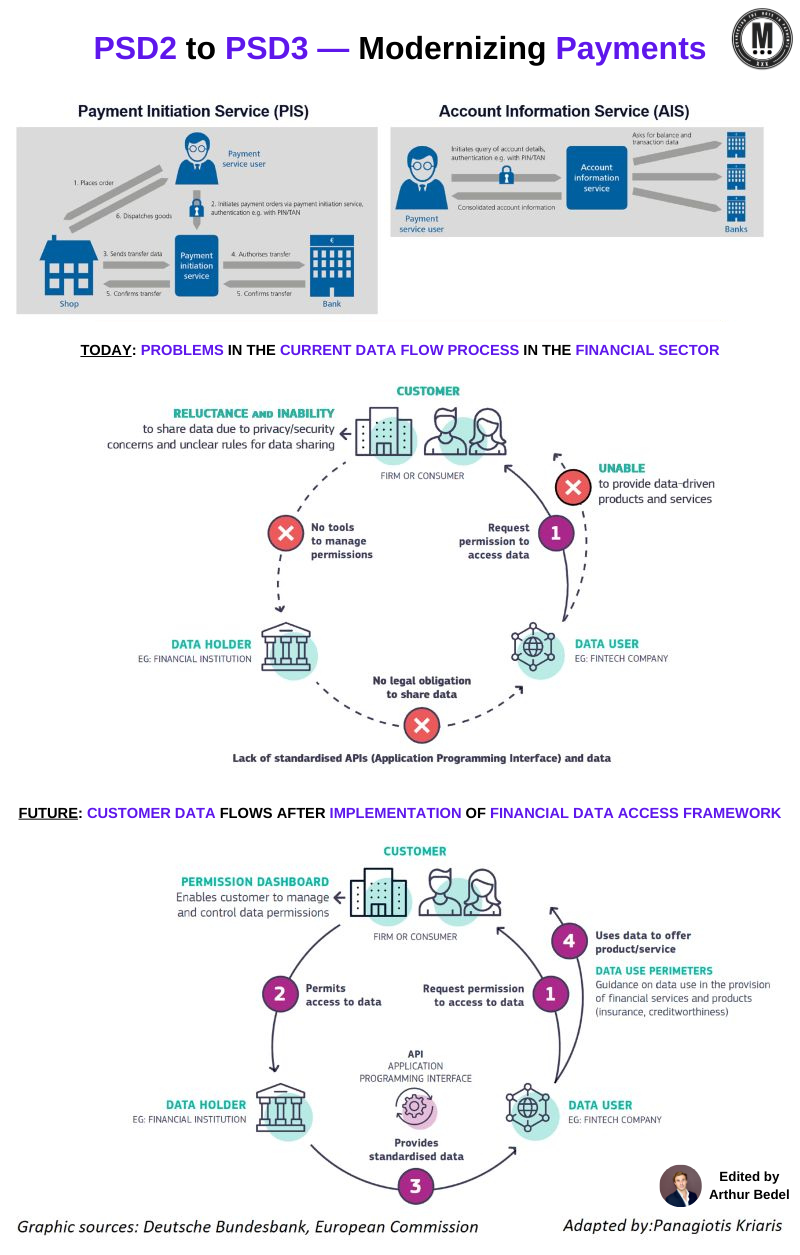

The European Commission has put forward proposals on the future of EU payments by modernizing the PSD2 legislation into PSD3👇

A series of developments have triggered the need for changes:

► The spectacular growth of electronic payments in the EU (30% in the 4 years until 2021 to 240€ trillion in value)

► New Fintech players entering the market or taking significant space (i.e. kevin., Satispay, Nuvei...)

►Open Banking (account information and payment initiation) opening up new use cases

► Innovation - Instant payments (SEPA), contactless (Tap to Pay by Apple + others) and QR codes taking a central stage

► PSD2 inefficiencies

The proposals can be summarized into 6 main blocks:

1️⃣ Open Banking improvements:

► New requirements for dedicated data access interfaces

► Banks will no longer need to maintain two data access interfaces

► Open banking providers to be given contingency data access

► All providers (banks and PSPs) to set up a "dashboard" for consumers to view, control (and be able to revoke) data access rights

► Obligation to provide access to financial data beyond payment account data

2️⃣ Fraud mitigation:

► Extend refund rights for fraud victims

► New mandatory system to match IBAN numbers with account names

► Stronger customer authentication rules

► A legal basis for PSPs to share fraud-related information between them

3️⃣ Fairer competition between banks and the 1000+ non-bank PSPs to drive down prices:

► Allow PSPs to access all EU payment systems

► Secure payment and e-money institutions' (there are 800 and 270 respectively) access to a bank account

4️⃣ Simplification:

► Merging e-money institutions (EMIs) with payment institutions (PIs) under one regime

► All payment rules applicable to PSPs will be contained in a directly applicable regulation

5️⃣ Improve the availability of cash in shops and via ATMs, by allowing retailers to provide cash services to customers without requiring a purchase and clarifying the rules for independent ATM operators

6️⃣ Improve consumer rights (i.e. when funds are blocked, improve transparency on account statements and ATM charges)

It's important to note that on top of PSD3 the above will be implemented by a Payment Services Regulation (PSR). The difference is that the former (PSD3) needs to be transposed into the national laws of all EU Member States, whereas the latter (PSR) is an EU Regulation, which will apply directly across all member states.

The PSR will regulate both Open Banking and PSPs, with the intention to create a more coherent, single legal framework across the EU that will, in turn, reduce the fragmentation coming from national legislations

Source: Deutsche Bank, European Commission and Panagiotis Kriaris

I highly recommend following my partner at Connecting the dots in payments... Arthur Bedel 💳 ♻️ for more great content like this one👌

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()